by

by The Time Value of Money (TVM) is a foundational concept in financial management stating that a rupee today is worth more than a rupee tomorrow. This is not due to inflation alone, but primarily because money available now can be invested to earn returns, making it grow over time. Conversely, receiving money in the future involves opportunity cost—the loss of potential earnings that could have been generated if the money were received earlier. TVM recognizes that money has a “time-dependent” value, meaning its purchasing power and growth potential change with time. Every financial decision—whether investing in a project, buying bonds, saving for retirement, or taking a loan—requires adjusting cash flows occurring at different points in time to a common date. Without applying TVM principles, comparing amounts across different time periods leads to flawed decisions. For example, ₹1,000 received today is clearly preferable to ₹1,000 received five years later, because today’s amount can be invested to become a larger sum in the future.

Three key factors drive TVM: the interest rate (return) , the time period, and the frequency of compounding. Higher interest rates and longer time periods magnify the difference between present and future values. TVM is mathematically expressed through two core calculations: Future Value (FV) , which answers “What will today’s money grow to?” using compounding; and Present Value (PV) , which answers “What is future money worth today?” using discounting. The basic formulas are FV = PV × (1 + r)^n and PV = FV / (1 + r)^n, where ‘r’ is the interest rate per period and ‘n’ is the number of periods. These formulas assume that interest earned is reinvested to earn further interest (compounding). Variations include annuities (equal periodic payments), perpetuities, and continuous compounding. Understanding these calculations allows financial managers to compare projects with different cash flow timings and choose the one that maximizes shareholder wealth.

TVM is the bedrock of almost all financial management decisions. In capital budgeting, it enables Net Present Value (NPV) and Internal Rate of Return (IRR) calculations, ensuring that project cash flows are discounted appropriately. In financing decisions, it helps compare loan offers with different interest rates and repayment schedules. For bond valuation, TVM discounts future coupon payments and principal to arrive at today’s fair price. In personal finance, it guides retirement planning (how much to save today for a target future corpus) and loan amortization schedules. Ignoring TVM leads to overvaluing future cash flows and accepting suboptimal investments. Ultimately, TVM reinforces the core principle of wealth maximization: a financial manager should only undertake actions where the present value of benefits exceeds the present value of costs. Every rupee must be evaluated not just by its face value, but by its timing.

|

Compounding |

Discounting |

|

| Meaning | The method used to determine the future value of present investment is known as Compounding. | The method used to determine the present value of future cash flows is known as Discounting. |

| Concept | If we invest some money today, what will be the amount we get at a future date. | What should be the amount we need to invest today, to get a specific amount in future. |

| Use of | Compound interest rate. | Discount rate |

| Known | Present Value | Future Value |

| Factor | Future Value Factor or Compounding Factor | Present Value Factor or Discounting Factor |

| Formula | FV = PV (1 + r)^n | PV = FV / (1 + r)^n |

Assumptions of Time Value of Money:

1. Money Can Be Invested Productively

TVM assumes that any amount of money available today can be invested immediately into an asset or project that generates a positive return (interest, profit, or growth). This is the most critical assumption—without the ability to earn a return, there would be no difference between receiving money today or later. The return could be from bank deposits, bonds, stocks, business operations, or any income-generating activity. This assumption justifies why a rupee today is worth more: it can start earning immediately. If investment opportunities do not exist (e.g., in a zero-interest economy or stagnant market), the time value concept collapses or becomes negligible.

2. Reinvestment of Intermediate Cash Flows

TVM calculations, particularly future value and compounding, assume that any interest, dividend, or cash flow received during the investment period will be reinvested at the same rate of return as the original investment. For example, if you earn ₹100 interest after one year, it is assumed that ₹100 will be reinvested and earn further interest in subsequent years. This assumption of reinvestment at a constant rate is necessary for compound growth formulas to hold true. In reality, reinvestment rates may fluctuate, but TVM theory assumes stability for mathematical convenience. Without reinvestment, compounding would not occur, and returns would be linear (simple interest).

3. Certainty of Cash Flows (No Risk)

Basic TVM models assume that future cash flows, interest rates, and time periods are known with absolute certainty. There is no default risk (the borrower will pay), no market risk (interest rates will not change unexpectedly), and no inflation risk (purchasing power erosion is ignored or separately accounted for). This assumption allows clean mathematical calculations of present and future values. In advanced finance, risk and uncertainty are incorporated through risk-adjusted discount rates or probability analysis, but the foundational TVM concept assumes a risk-free world. Real-world financial managers must modify TVM by adding risk premiums to discount rates.

4. Rational Investor Behavior

TVM assumes that investors and financial managers are rational—they prefer more wealth to less and prefer receiving money earlier rather than later, all else being equal. Rationality means that given a choice between ₹1,000 today and ₹1,000 one year from now, every rational person will choose today’s amount. This assumption underpins the concept of positive time preference: people value present consumption/wealth more than future consumption. Rational investors will only delay receiving money if they are compensated with additional returns (interest). Without rational preference for earlier money, the entire framework of discounting and compounding loses its behavioral foundation.

5. Constant or Known Interest Rate (r)

TVM calculations assume that the interest rate (discount rate or compounding rate) remains constant over the entire time period or is known in advance for each period. This rate represents the opportunity cost of funds—what you could earn elsewhere. Whether using future value (FV = PV × (1+r)^n) or present value (PV = FV / (1+r)^n), the rate ‘r’ is treated as fixed. In reality, interest rates fluctuate due to monetary policy, inflation, and market forces. However, the assumption of a constant rate simplifies mathematics and allows comparison of different investment options. Advanced TVM models may use variable rates, but basic theory assumes stability for clarity and tractability.

6. Discrete Compounding Periods

Standard TVM assumes that compounding (or discounting) occurs at discrete, regular intervals—annually, semi-annually, quarterly, monthly, or daily. The formula FV = PV × (1 + r/n)^(n×t) explicitly assumes ‘n’ equal sub-periods per year. This assumption implies that interest is calculated and added to principal only at the end of each interval, not continuously. While continuous compounding (using the mathematical constant ‘e’) exists as an extension, basic TVM assumes discrete periods because most real-world financial contracts (bank deposits, loan EMIs, bond coupons) specify periodic interest calculations. The assumption of discrete periods makes calculations practical and aligns with standard accounting and contractual practices.

7. No Transaction Costs or Taxes (Simplified Model)

Basic TVM theory assumes that there are no costs associated with investing, withdrawing, or transferring money—no brokerage fees, no transaction charges, no taxes on interest income, and no inflation erosion. This assumption allows a pure focus on the time value itself. In reality, taxes on interest (e.g., TDS on bank deposits) and transaction fees reduce net returns, while inflation reduces purchasing power. Financial managers adjust for these factors separately by using after-tax discount rates or real (inflation-adjusted) rates. However, the core TVM concept assumes a frictionless environment where every rupee earned in interest is fully retained and reinvested without leakage.

8. Unlimited Divisibility of Money

TVM assumes that money can be divided into any small unit and invested in fractional amounts. For example, if you have ₹1,000 and an investment requires a minimum of ₹10,000, basic TVM theory ignores such practical restrictions and assumes you can invest any portion. Similarly, interest calculations assume that even a single rupee can earn the same rate as a large sum. This assumption of perfect divisibility allows continuous formulas and simplifies analysis. In reality, many investments (real estate, fixed deposits with minimum balances, bond lots) have minimum size requirements. However, for theoretical and most classroom purposes, money is assumed infinitely divisible, enabling clean TVM mathematics without lumpiness constraints.

Present Value and Future Value:

While compounding value for the depreciation of the assets, you need to keep in mind two important values: present value and future value. Future value is the value of the asset after a certain time period. While the present value is the value of the asset that we calculate after deducting the residual value.

FV = PV(1 + r)n

where FV= future value,PV = present value, r = rate of interest, n = equal number of periods.

PV = FV / (1 + r)n

Compounding

For understanding the concept of compounding, first of all, you need to know about the term future value. The money you invest today, will grow and earn interest on it, after a certain period, which will automatically change its value in future. So the worth of the investment in future is known as its Future Value. Compounding refers to the process of earning interest on both the principal amount, as well as accrued interest by reinvesting the entire amount to generate more interest.

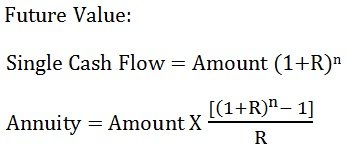

Compounding is the method used in finding out the future value of the present investment. The future value can be computed by applying the compound interest formula which is as under:

Where n = number of years

R = Rate of return on investment.

Discounting

Discounting is the process of converting the future amount into its Present Value. Now you may wonder what is the present value? The current value of the given future value is known as Present Value. The discounting technique helps to ascertain the present value of future cash flows by applying a discount rate. The following formula is used to know the present value of a future sum:

Where 1,2,3,…..n represents future years

FV = Cash flows generated in different years,

R = Discount Rate

One thought on “Time Value of Money, Present, Future Value of Money”