by

by Yield to Maturity (YTM)

YTM stands for “Yield to Maturity.” It is a financial metric used to assess the total return an investor can expect to receive from a fixed-income investment, such as a bond, if the investment is held until its maturity date. YTM takes into account the bond’s current market price, its face value (par value), the coupon interest payments, and the time remaining until maturity.

YTM is expressed as an annual percentage rate and provides a more comprehensive measure of the potential return on a bond compared to just considering its coupon rate. It considers not only the regular interest payments (coupon payments) but also any potential capital gain or loss resulting from the difference between the bond’s purchase price and its face value at maturity.

Calculating YTM can be complex, especially for bonds with varying coupon payments or those subject to call provisions or early redemption. The formula for calculating YTM involves solving for the discount rate that equates the present value of all future cash flows (coupon payments and face value) with the bond’s current market price.

Points about YTM:

- Coupon Rate vs. YTM: The coupon rate is the fixed interest rate the bond pays on an annual basis, while YTM takes into account the total return including coupon payments, capital gains or losses, and the time value of money.

- Price and YTM Relationship: When the market price of a bond is equal to its face value, the YTM is equal to the coupon rate. If the bond is trading at a premium (above face value), the YTM will be lower than the coupon rate. If the bond is trading at a discount (below face value), the YTM will be higher than the coupon rate.

- Investment Decision: YTM is a useful metric for comparing different bond investment opportunities and assessing their potential returns. Investors often seek bonds with higher YTM when looking for better potential returns.

- YTM Assumptions: YTM assumes that all coupon payments are reinvested at the YTM rate until maturity. This might not reflect actual market conditions.

- Interest Rate Impact: YTM is sensitive to changes in prevailing interest rates. When interest rates rise, the value of existing bonds with fixed coupon rates tends to decrease, resulting in a higher YTM.

TYM Formula

The Yield to Maturity (YTM) of a bond is calculated by solving for the discount rate that equates the present value of all future cash flows (coupon payments and face value) with the current market price of the bond. The formula for YTM is complex and involves iterative calculations. However, you can use financial calculators, spreadsheet software, or online calculators to compute YTM efficiently. Here’s the formula:

YTM Importance

- Assessment of Potential Return: YTM provides a comprehensive assessment of the potential return an investor can expect from a bond if it’s held until maturity. It considers both the coupon payments and any capital gain or loss resulting from the difference between the bond’s purchase price and its face value at maturity.

- Investment Comparison: YTM allows investors to compare different bonds with varying coupon rates, maturities, and market prices on an equal basis. This standardized measure helps investors assess which bonds offer better potential returns relative to their risk profiles.

- Informed Investment Decisions: YTM assists investors in making informed investment decisions. By considering both current income (coupon payments) and capital appreciation (if applicable), investors can better evaluate the attractiveness of different bonds.

- Understanding Interest Rate Impact: YTM helps investors understand the impact of changes in market interest rates on bond valuations. When market rates rise, the value of existing bonds with fixed coupon rates tends to decrease, potentially leading to capital losses.

- Comparison to Required Returns: YTM serves as a benchmark for comparing the potential return of a bond with the investor’s required rate of return or cost of capital. If a bond’s YTM is higher than the investor’s required return, it may be considered an attractive investment.

- Portfolio Diversification: YTM assists in portfolio diversification by allowing investors to allocate funds to bonds with different yield characteristics. Investors can balance their portfolios based on both risk and return.

- Sensitivity Analysis: YTM can be used in sensitivity analysis to assess the potential impact of interest rate changes on bond valuations. This helps investors anticipate how their bond holdings might perform in different interest rate environments.

- Basis for Valuation: YTM is a fundamental component of bond valuation. It’s often used in the context of determining the fair market value of bonds when considering buying or selling decisions.

- Risk Consideration: YTM indirectly factors in risk by accounting for the time value of money. Higher-risk bonds typically offer higher YTM to compensate investors for the additional risk.

- Strategic Planning: YTM is valuable for long-term strategic planning and investment strategies. It guides investors in choosing bonds that align with their financial goals and risk tolerance.

- Credit and Market Risk Assessment: Although YTM doesn’t directly consider credit risk, it can provide insight into the relative riskiness of different bonds by comparing their yield levels.

Advantages of YTM:

- Comprehensive Return Measure: YTM provides a comprehensive measure of the potential return on a bond investment by considering both coupon payments and the potential capital gain or loss upon maturity.

- Standardized Comparison: YTM allows for easy comparison of different bonds with varying coupon rates, maturities, and market prices. It standardizes the assessment of potential returns.

- Objective Investment Decision: YTM assists investors in making objective investment decisions by quantifying the potential return for holding a bond until maturity.

- Accounting for Time Value of Money: YTM accounts for the time value of money, recognizing that future cash flows are worth less than present cash flows, due to factors like inflation and opportunity cost.

- Useful for Portfolio Diversification: YTM helps investors diversify their portfolios by comparing bonds with differing characteristics and choosing those that align with their return expectations and risk tolerance.

- Sensitivity Analysis: YTM can be used to perform sensitivity analysis, assessing how changes in market interest rates impact the potential return of a bond.

- Benchmark for Required Return: YTM serves as a benchmark for investors to compare the potential return of a bond with their required rate of return or cost of capital.

Disadvantages of YTM:

- Assumption of Maturity: YTM assumes that the bond will be held until maturity and that all coupon payments will be reinvested at the calculated YTM rate, which might not reflect the investor’s actual actions.

- Interest Rate Changes: YTM calculations are sensitive to changes in market interest rates. If market rates rise, the value of existing bonds with fixed coupon rates will decrease, potentially leading to different actual returns.

- Complex Calculation: Calculating YTM manually involves iterative calculations, which can be complex and time-consuming. However, financial calculators and spreadsheet software simplify the process.

- Reinvestment Assumption: The assumption that coupon payments will be reinvested at the YTM rate might not reflect real-world investment opportunities and can impact the actual return.

- Lack of Consideration for Risk: YTM doesn’t directly account for credit risk, inflation risk, or other risks associated with bond investments.

- Discount Rate Estimation: Estimating an appropriate discount rate (YTM) can be subjective and might vary among investors. A small change in the discount rate can significantly impact the calculated YTM.

- Terminal Value Estimation: YTM might not accurately capture the value of long-term bonds with varying cash flows or complex structures.

- Doesn’t Reflect Real-time Market Prices: YTM is based on the bond’s current market price, which may be different from the actual price an investor pays due to market fluctuations and transaction costs.

Internal Rate of Return (IRR)

IRR stands for “Internal Rate of Return.” It is a financial metric used to assess the potential profitability of an investment or project. IRR represents the discount rate at which the net present value (NPV) of the investment’s cash flows becomes zero. In other words, it is the rate at which the present value of the investment’s expected future cash flows equals the initial investment amount.

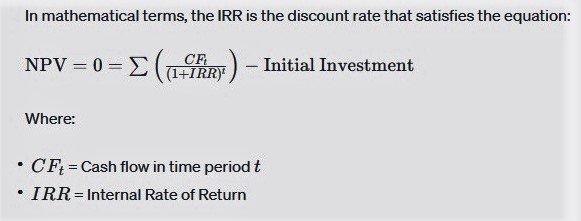

In mathematical terms, the IRR is the discount rate that satisfies the equation:

Key points about IRR:

- Profitability Measure: IRR is used to evaluate whether an investment or project is expected to generate a satisfactory return. If the calculated IRR is higher than the required rate of return or cost of capital, the investment may be considered financially attractive.

- Comparison to Required Return: Similar to the cost of capital, the IRR represents the minimum rate of return required for an investment to be worthwhile. If the IRR is greater than the cost of capital, the investment may be acceptable.

- Relative Comparison: IRR is useful for comparing multiple investment opportunities with differing cash flows and timelines. The investment with the highest IRR is generally preferred, assuming all other factors are equal.

- Solving for IRR: Calculating IRR involves finding the discount rate that makes the NPV of cash flows equal to zero. This is typically done through iterative calculations or by using financial calculators and software.

- Multiple IRRs: Some investment scenarios may result in multiple possible IRRs or no real solution. In such cases, the IRR measure might not be as reliable.

- Cash Flow Patterns: The IRR assumes that cash flows generated by the investment are reinvested at the same IRR rate. This assumption might not hold in practice.

- Non-Conventional Cash Flows: The presence of non-conventional cash flows (e.g., negative cash flows followed by positive cash flows) can lead to challenges in calculating IRR.

- Potential Misleading Results: In some cases, IRR may yield misleading results, especially when comparing projects with different cash flow patterns or when considering mutually exclusive projects.

- Risk Consideration: The IRR implicitly accounts for the time value of money and risk, but it doesn’t explicitly quantify the risk associated with an investment.

- Dependence on Assumptions: Like other financial metrics, IRR depends on the accuracy of input assumptions, including cash flow projections and discount rates.

IRR Uses

- Investment Evaluation: IRR is commonly used to evaluate the potential profitability of investment projects, such as capital expenditures, new product developments, acquisitions, and other business ventures. It helps assess whether the expected returns from an investment exceed the required rate of return or cost of capital.

- Project Ranking and Selection: When there are multiple investment options, IRR provides a basis for comparing and ranking projects. The project with the highest IRR is often considered the most attractive, assuming all other factors are equal.

- Capital Budgeting: IRR is a critical tool in capital budgeting decisions. It assists in determining which projects should receive funding and helps allocate resources efficiently.

- Real Estate Analysis: IRR is used in real estate investment analysis to evaluate the potential returns from purchasing properties, developing real estate projects, or renting out properties.

- Equity Investment Assessment: For equity investors, IRR helps assess the potential returns from investments in stocks or private equity. It assists in determining whether an investment is likely to achieve the desired return.

- Private Equity and Venture Capital: In the context of private equity and venture capital investments, IRR is used to evaluate the potential returns from investing in startups, growth-stage companies, and other private enterprises.

- Loan or Debt Investment Analysis: Lenders use IRR to assess the potential returns from lending money or investing in debt instruments. It helps them make decisions about lending terms and risk exposure.

- Financial Product Evaluation: IRR is applied in evaluating financial products like bonds, certificates of deposit (CDs), and other fixed-income instruments to determine whether the potential returns align with investor objectives.

- Infrastructure and Public Projects: Public sector projects, such as infrastructure developments, also use IRR to assess the feasibility and potential economic benefits of large-scale initiatives.

- Private Investment Funds: Investors in private investment funds, such as hedge funds or private equity funds, use IRR to understand the potential returns from their investments over the fund’s holding period.

- Comparison to Market Returns: Investors compare the IRR of potential investments with the historical returns of market indices or benchmark rates to make informed investment decisions.

- Risk Assessment: While IRR does not explicitly quantify risk, it does implicitly consider the time value of money and risk in its calculations. This makes it a tool for assessing the risk-reward trade-off in investment opportunities.

IRR Types

- Simple IRR: This is the standard IRR calculation used for conventional cash flows, where there is an initial investment followed by a series of positive cash inflows. It’s the most widely used type of IRR for evaluating investment projects.

- Modified IRR (MIRR): MIRR is an alternative to the standard IRR that addresses some of the limitations of the traditional IRR calculation. MIRR assumes that cash flows are reinvested at a specified reinvestment rate, which is often more realistic than assuming they are reinvested at the IRR rate. MIRR accounts for both the cost of capital for financing and a realistic reinvestment rate for returns.

- Multiple IRR: In some cases, an investment may have more than one IRR, particularly if there are changing cash flow patterns (e.g., multiple sign changes). When multiple IRRs are present, it can complicate the interpretation and application of the IRR metric.

- Negative IRR: Negative IRR indicates that the investment is expected to result in a loss. This can happen when the initial investment is high and the expected cash flows are insufficient to recover the investment.

- Non–Conventional Cash Flows: Non-conventional cash flows involve a combination of positive and negative cash flows over time, such as an initial investment followed by alternating periods of inflows and outflows. Calculating IRR for non-conventional cash flows can be challenging and may lead to multiple IRRs.

- Continuous Compounding IRR: While the standard IRR assumes discrete compounding of cash flows, the continuous compounding IRR calculates the rate at which the present value of the future cash flows equals the initial investment amount under continuous compounding assumptions.

- Modified Dietz IRR: This IRR type is used in the context of investment performance measurement, particularly for portfolios with changing cash flows and valuation dates. It considers the timing and amount of cash flows when calculating the rate of return.

- Effective Annual Rate (EAR): The EAR, also known as the annual equivalent rate (AER) or effective annual yield (EAY), represents the annualized rate of return when compounding occurs more frequently than annually. It accounts for the compounding frequency to provide a more accurate measure of returns.

- Real IRR: Real IRR adjusts the nominal IRR for inflation, providing a measure of the investment’s actual purchasing power increase.

- Sector–Specific IRR: Different sectors, industries, or projects may have specific methods for calculating IRR based on unique cash flow patterns, regulations, or industry practices.

Advantages of IRR:

- Comprehensive Measure of Return: IRR provides a comprehensive measure of the potential return on an investment, considering both the timing and magnitude of cash flows.

- Relative Investment Comparison: IRR allows for the comparison of different investment opportunities with varying cash flow patterns, durations, and sizes. The investment with the highest IRR is generally preferred, assuming all other factors are equal.

- Incorporates Time Value of Money: IRR takes into account the time value of money by discounting future cash flows back to their present value, helping investors assess the opportunity cost of their investments.

- Easy to Communicate: IRR is expressed as a percentage rate, making it easy to communicate and understand by investors, analysts, and decision-makers.

- Objective Investment Decisions: When compared to a required rate of return or cost of capital, IRR helps in making objective investment decisions. If the IRR exceeds the required return, the investment may be considered acceptable.

- Intuitive Measure: IRR is an intuitive measure that resonates with the concept of investment returns. Investors often prefer higher IRR values.

Disadvantages of IRR:

- Multiple IRRs: For projects with non-conventional cash flows (e.g., multiple sign changes), there can be multiple IRRs or no real solution, leading to confusion and uncertainty in interpretation.

- Inconsistent Ranking for Mutually Exclusive Projects: IRR may lead to inconsistent project rankings when comparing mutually exclusive projects with different investment sizes or cash flow patterns.

- Reinvestment Assumption: IRR assumes that cash flows are reinvested at the same IRR rate, which might not accurately reflect real-world investment opportunities.

- Unreliable for Large Negative Cash Flows: If an investment involves a large initial cash outflow followed by smaller positive cash flows, IRR can be misleading and might not accurately represent the potential profitability.

- Misleading with Non-Conventional Cash Flows: IRR can produce unrealistic results when applied to projects with non-conventional cash flows (e.g., alternating inflows and outflows), leading to difficulties in interpretation.

- Lack of Risk Quantification: IRR doesn’t explicitly quantify risk, and two projects with the same IRR might have different levels of risk associated with their cash flows.

- Dependence on Assumptions: Like other financial metrics, IRR is dependent on assumptions, including cash flow projections and discount rates. Small changes in these inputs can lead to significant changes in the calculated IRR.

- No Measure of Absolute Value: While IRR indicates the potential return, it doesn’t provide information about the actual dollar value of the investment’s returns, making it difficult to compare across different investments.

- Less Accurate for Comparing Short and Long-Term Investments: IRR can give misleading results when comparing projects with vastly different durations, as it doesn’t consider the absolute dollar amounts of returns.

- Sensitivity to Changes in Cash Flows: IRR calculations are sensitive to changes in cash flows, and small variations in projected cash flows can lead to significantly different IRR values.

Important Differences between YTM and IRR

|

Basis of Comparison |

Yield to Maturity (YTM) |

Internal Rate of Return (IRR) |

| Definition | YTM is the discount rate that makes the NPV of cash flows equal to the bond’s current market price. | IRR is the discount rate that makes the NPV of cash flows equal to zero, indicating breakeven. |

| Application | Used to evaluate the potential return of bonds and fixed-income securities. | Used to evaluate the potential return of various investments, including projects and ventures. |

| Investment Type | Typically applied to fixed-income securities like bonds. | Applied to various investment opportunities, including projects, ventures, and equity investments. |

| Cash Flow Patterns | YTM assumes a set schedule of coupon payments and a single repayment of the face value at maturity. | IRR can handle non-conventional cash flows, including changing signs and multiple sign changes. |

| Investment Duration | Often used for evaluating longer-term investments like bonds with fixed maturities. | Applicable to investments with varying durations, including short-term and long-term projects. |

| Calculating Process | YTM is typically calculated using iterative methods or financial calculators. | IRR is calculated using iterative methods or specialized software, aiming for an NPV of zero. |

| Comparison to Required Return | YTM is compared to a required rate of return or cost of capital. | IRR is compared to the required rate of return to determine project viability. |

| Decision Rule | If YTM is higher than the required return, the bond may be considered attractive. | If IRR is higher than the required return, the project may be considered acceptable. |

| Multiple Solutions | YTM has a single solution for conventional cash flows. | IRR might have multiple solutions or no real solution for certain cash flow patterns. |

| Investment Size | Suitable for analyzing individual bonds or fixed-income securities. | Suitable for analyzing projects or investments with varying sizes and cash flow patterns. |

| Sensitivity to Interest Rate Changes | YTM provides insight into the impact of interest rate changes on bond valuations. | IRR indicates the rate at which NPV equals zero, capturing interest rate impacts on returns. |

| Reinvestment Assumption | YTM assumes reinvestment of coupon payments at the YTM rate. | IRR assumes reinvestment of cash flows at the IRR rate. |

| Objective | To evaluate the potential returns from holding a bond until maturity. | To evaluate the potential returns from various investments over their respective timeframes. |

| Use in Investment Decision-Making | Helps investors decide whether to purchase or hold a bond based on potential returns. | Assists investors in choosing between competing investment opportunities. |

| Risk Consideration | YTM indirectly considers the risk by accounting for the time value of money. | IRR doesn’t explicitly quantify risk but considers returns relative to required return. |

Similarities between YTM and IRR

- Return Measurement: Both YTM and IRR are used to measure the potential return on an investment. They provide insights into the profitability of an investment by considering the timing and magnitude of cash flows.

- Discounted Cash Flows: Both metrics involve discounting future cash flows back to their present value. YTM discounts the bond’s future coupon payments and face value, while IRR discounts investment project cash flows.

- Interest Rate Sensitivity: Both YTM and IRR are sensitive to changes in interest rates. Changes in interest rates can impact the calculated values of both metrics and influence investment decisions.

- Financial Decision-Making: Both metrics assist investors and decision-makers in evaluating the attractiveness of an investment. YTM helps bondholders determine whether a bond is a good investment, while IRR helps evaluate whether a project or venture is worthwhile.

- Comparison to Required Rate: Both YTM and IRR are compared to a required rate of return. If YTM is higher than the required return, the bond may be considered attractive. If IRR is higher than the required return, the investment project may be acceptable.

- Benchmark for Acceptance: Both metrics have benchmark values that influence investment decisions. If YTM or IRR exceeds the required rate of return or cost of capital, the investment is more likely to be accepted.

- Calculation Assumptions: Both YTM and IRR make assumptions about the reinvestment of cash flows. YTM assumes reinvestment of coupon payments at the YTM rate, while IRR assumes reinvestment at the IRR rate.

- Time Value of Money: Both metrics consider the time value of money by discounting future cash flows. They recognize that money received in the future is worth less than money received today.

- Financial Goal Alignment: Both YTM and IRR are used to align investment decisions with financial goals. They provide quantitative measures for evaluating whether an investment aligns with the desired returns and risk tolerance.

- Standardized Measurement: Both YTM and IRR provide standardized measures of potential returns, making it easier to compare and evaluate different investment opportunities.

Advisory Note: Article shared based on knowledge available on internet and for the Knowledge purpose only. Please contact Professional/Advisor/Doctor for treatment/Consultation.

Articles on intactone.com are general information, and are not intended to substitute for Professional Advice. The information is “AS IS”, “WITH ALL FAULTS”. User assumes all risk of Use, Damage, or Injury. You agree that we have no liability for any damages.