by

by Opportunity Cost

Opportunity cost refers to the value of the next best alternative that must be forgone when a decision is made to allocate resources, such as time, money, and effort, to a particular course of action. It’s a fundamental concept in economics and business decision-making that helps assess the trade-offs involved in various choices.

- Investment Choices: A company might have the option to invest its available funds in expanding its product line or upgrading its manufacturing facilities. The opportunity cost would be the potential returns and growth that could have been achieved by choosing the other investment option.

- Resource Allocation: A business might need to decide whether to allocate its workforce to work on a high-priority project or a lower-priority project. The opportunity cost would be the potential benefits and revenue that could have been generated from the alternative project.

- Time Management: An entrepreneur might choose to spend time attending networking events instead of focusing on product development. The opportunity cost would be the potential advancements in product development that could have been achieved with that time.

- Pricing Decisions: When setting prices for products or services, a company might need to consider the opportunity cost of setting prices too low (losing potential revenue) or too high (potentially losing customers).

- Supplier Selection: When selecting suppliers, a business might need to weigh the opportunity cost of choosing a lower-cost supplier against potential quality or reliability issues.

- Location Decisions: When choosing a business location, a company might need to consider the opportunity cost of selecting a location that offers lower costs but potentially limited access to customers.

Characteristics of Opportunity Cost

Opportunity cost possesses several key characteristics that help illustrate its nature and importance in decision-making and resource allocation:

- Trade-offs: Opportunity cost arises due to the limited availability of resources and the need to make choices. When one option is chosen, other alternatives must be forgone, leading to trade-offs.

- Subjectivity: The value of opportunity cost can vary from person to person and situation to situation. Different individuals may assign different values to the same alternatives based on their preferences, goals, and circumstances.

- Decision Focus: Opportunity cost highlights the focus on the next best alternative that is given up when a decision is made. It directs attention to what could have been gained if a different choice had been made.

- Comparative Nature: Opportunity cost is determined by comparing the benefits of one choice to the benefits of the best alternative. It’s not an absolute value but rather a relative assessment.

- Future-Oriented: Opportunity cost relates to future potential gains rather than sunk costs. It emphasizes the benefits that could be obtained by choosing the best alternative for a specific purpose.

- Implicit Costs: Opportunity cost includes both explicit costs (monetary expenses) and implicit costs (value of resources given up). Implicit costs may include time, effort, and other non-monetary sacrifices.

- Quantitative and Qualitative: Opportunity cost can be expressed quantitatively, such as in monetary terms, or qualitatively, considering non-monetary benefits or drawbacks.

- Economic Rationality: Decision-makers are assumed to act rationally by considering opportunity cost to maximize their benefits when making choices.

- Long-Term Implications: Assessing opportunity cost encourages decision-makers to consider the long-term effects of their choices and avoid making decisions solely based on immediate gains.

- Influence on Decision-Making: Opportunity cost affects how individuals, businesses, and policymakers evaluate alternatives and prioritize resource allocation.

- Context-Dependent: The determination of opportunity cost depends on the context of the decision, the available alternatives, and the specific objectives.

- Dynamic: As circumstances change, the opportunity cost associated with a particular choice may also change.

How to Calculate Opportunity Costs?

Calculating opportunity costs involves comparing the benefits of choosing one option over another and identifying what you’re giving up by making that choice. The process may vary depending on the context and the available alternatives. Here’s a general framework for calculating opportunity costs:

- Identify the Decision: Clearly define the decision you need to make and the alternatives you’re considering.

- List Benefits: Make a list of the potential benefits or gains associated with each alternative. These could be monetary, time-related, or any other relevant factor.

- Quantify Benefits: If possible, assign a monetary value to the benefits for each alternative. This helps create a basis for comparison.

- Identify Next Best Alternative: Determine the next best alternative that you’re giving up by choosing a particular option.

- List Costs: Make a list of the potential costs or drawbacks associated with the next best alternative. Again, quantify these if possible.

- Calculate Opportunity Cost: Subtract the benefits of the chosen option from the benefits of the next best alternative. This gives you the opportunity cost in monetary terms.

- Evaluate Non-Monetary Factors: Consider any non-monetary factors that influence your decision. These could include personal preferences, time commitments, or qualitative considerations.

- Decision Assessment: Analyze whether the benefits of the chosen option outweigh the opportunity cost. Assess whether the benefits align with your goals and priorities.

Here’s a simplified example to illustrate how to calculate opportunity cost:

Scenario:

You have two part-time job offers. Job A pays $20 per hour, and Job B pays $25 per hour. However, Job A is closer to your home, saving you a 30-minute commute each way.

- Identify Decision: Choose between Job A and Job B.

- List Benefits: Job A: $20/hour, shorter commute. Job B: $25/hour.

- Quantify Benefits: Assign a value of $10 to the time saved from the shorter commute for Job A.

- Identify Next Best Alternative: The next best alternative for Job A is Job B.

- List Costs: Job B: Longer commute, potential time loss.

- Calculate Opportunity Cost: For Job A: $20 + $10 = $30/hour. For Job B: $25/hour.

- Evaluate Non-Monetary Factors: Consider how important the shorter commute is to you.

- Decision Assessment: Decide whether the opportunity cost of earning $5 less per hour with Job A is worth the time saved on the commute.

Advantages of Opportunity Costs:

- Informed Decision-Making: Understanding opportunity costs helps individuals and businesses make more informed choices by evaluating trade-offs and potential gains.

- Resource Allocation: It assists in allocating limited resources (time, money, effort) effectively by choosing alternatives that align with goals.

- Strategic Planning: Businesses can develop effective strategies by considering the long-term implications and benefits of different options.

- Maximizing Benefits: By comparing benefits and drawbacks, decision-makers can aim to maximize benefits and minimize losses.

- Rational Decisions: It promotes rational decision-making, as individuals weigh the potential benefits of each alternative.

- Long-Term Perspective: Focusing on opportunity costs encourages a long-term perspective rather than making decisions based solely on immediate gains.

- Efficient Resource Use: Opportunity cost analysis aids in using resources efficiently and avoiding wasteful choices.

Disadvantages of Opportunity Costs:

- Complexity: Calculating opportunity costs can be complex, particularly when non-monetary factors are involved.

- Subjectivity: Assigning values to benefits and drawbacks can be subjective, leading to different assessments by different individuals.

- Incomplete Information: In some cases, the true value of alternatives may be uncertain, making accurate calculation difficult.

- Overanalysis: Overthinking opportunity costs might lead to decision paralysis or excessive time spent on analysis.

- Limited Accuracy: The accuracy of monetary valuations depends on assumptions and estimations.

- Resource Constraints: Focusing solely on opportunity costs might overlook practical limitations or constraints that impact decision-making.

- Neglect of Non-Monetary Factors: Overemphasizing monetary benefits may neglect qualitative factors that are important in decision-making.

- Complexity for Businesses: In a business context, opportunity cost calculations can be complex, especially when multiple factors are involved.

- Time-Consuming: Calculating opportunity costs can take time, which might not be feasible for quick decisions.

Marginal Cost

Marginal cost refers to the additional cost incurred by producing one more unit of a good or service. It’s a fundamental concept in economics that helps businesses and individuals analyze production and consumption decisions.

- Incremental Cost: Marginal cost focuses on the change in total cost resulting from producing or consuming one additional unit of a good or service.

- Variable Costs: Marginal cost is primarily driven by variable costs—costs that change with the level of production, such as raw materials, labor, and energy.

- Diminishing Returns: In many cases, as production increases, marginal cost tends to rise due to the principle of diminishing marginal returns. This means that adding more units of input (like labor) to a fixed amount of resources (like machinery) eventually leads to lower additional output and higher costs.

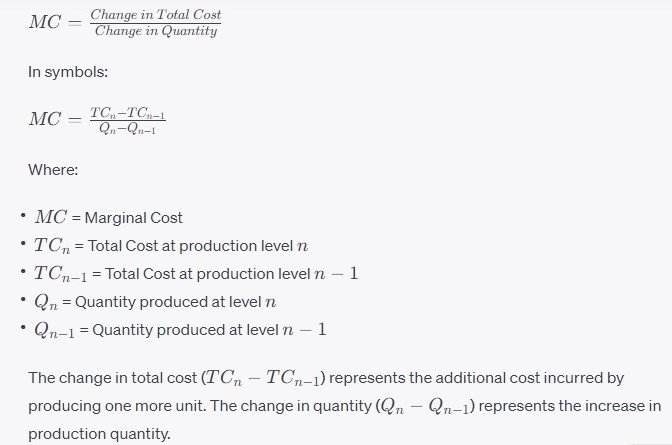

- Calculation: Marginal cost is calculated by dividing the change in total cost by the change in quantity produced. Mathematically, it’s expressed as: Marginal Cost = Change in Total Cost / Change in Quantity.

- Decision-Making: Businesses often consider marginal cost when deciding whether to increase production. If marginal cost is lower than the price at which the product can be sold, it may be profitable to produce more units.

- Equilibrium in Competitive Markets: In perfectly competitive markets, firms tend to produce where marginal cost equals the market price, as this maximizes their profit.

- Optimal Production Level: Understanding marginal cost helps businesses determine the optimal level of production that maximizes their profitability.

- Short-Run vs. Long-Run: Marginal cost is more relevant in the short run when variable inputs can be adjusted, as fixed costs remain constant in the short run.

- Sunk Costs: Sunk costs, which are costs that have already been incurred and cannot be recovered, are not considered in marginal cost calculations.

- Cost Efficiency: Monitoring marginal costs helps identify cost efficiency opportunities and potential areas for cost reduction.

Marginal cost formula

The formula for calculating marginal cost (MC) is straightforward. It involves finding the change in total cost (TC) when producing one additional unit of a good or service. Mathematically, it’s expressed as:

Example of marginal cost

Scenario:

A bakery produces cupcakes. The bakery’s fixed costs, which include rent, utilities, and equipment depreciation, amount to $1,000 per month. The variable costs, such as flour, sugar, and labor, increase as more cupcakes are produced.

- Production Level: Initially, the bakery produces 100 cupcakes per day.

- Total Cost: At 100 cupcakes per day, the total cost is $1,000 (fixed costs) + $300 (variable costs) = $1,300.

- Marginal Cost: To produce an additional 10 cupcakes, the total cost increases to $1,500. Therefore, the marginal cost of producing 10 additional cupcakes is $200 ($1,500 – $1,300).

As production increases, variable costs rise due to the need for more ingredients and additional labor. This leads to an increase in marginal cost. If the bakery continues to produce more cupcakes, the marginal cost will likely continue to rise due to the principle of diminishing marginal returns. Eventually, it might reach a point where adding more cupcakes becomes less cost-effective.

Mechanics of Marginal Costs

The mechanics of marginal cost involve understanding how the additional cost of producing one more unit of a product changes as production levels increase.

- Cost Components: Total costs comprise fixed costs and variable costs. Fixed costs remain constant regardless of production levels, while variable costs change with the quantity produced.

- Calculate Total Cost: Calculate the total cost of producing a certain quantity of units. This involves summing up fixed costs and variable costs for that level of production.

- Calculate Total Cost for One More Unit: Calculate the total cost of producing one more unit beyond the current quantity. This involves adding the variable cost associated with producing that additional unit to the total cost.

- Calculate Marginal Cost: The marginal cost is the difference between the total cost of producing one more unit and the total cost of producing the previous quantity. Mathematically, it’s expressed as: Marginal Cost = Change in Total Cost / Change in Quantity.

- Interpret Marginal Cost: Analyze the calculated marginal cost value. If it’s increasing, it implies that producing additional units is becoming more expensive due to diminishing returns or increased resource usage.

- Production Decision: Businesses compare the marginal cost with the price they can sell their product for. If the price is greater than the marginal cost, producing additional units is likely profitable. If the price is less than the marginal cost, it might not be cost-effective to produce more units.

- Optimal Production Level: In a competitive market, businesses aim to produce where marginal cost equals the market price. This maximizes their profit.

- Impact of Fixed Costs: In the short run, when fixed costs remain constant, marginal cost is primarily driven by changes in variable costs. In the long run, all costs become variable, affecting the behavior of marginal cost.

- Diminishing Returns: As production increases, marginal cost tends to rise due to the principle of diminishing marginal returns. This occurs when adding more units of input (like labor) leads to smaller increases in output and higher costs.

- Cost Efficiency: Analyzing marginal cost helps identify areas where production can be optimized for cost efficiency.

Advantages of Marginal Cost Analysis:

- Informed Production Decisions: Businesses can use marginal cost analysis to determine the optimal level of production that maximizes profitability.

- Resource Allocation: Helps allocate resources efficiently by identifying points where producing additional units becomes cost-ineffective.

- Pricing Strategy: Businesses can set prices based on marginal cost to ensure that prices cover variable costs and contribute to covering fixed costs.

- Profit Maximization: Maximizing profit involves producing where marginal cost equals marginal revenue, which helps achieve optimal profitability.

- Decision-Making: Provides a clear framework for evaluating production and pricing decisions, enhancing decision-makers’ understanding of trade-offs.

- Efficiency Improvement: Identifying diminishing returns points out where resource allocation can be adjusted to achieve greater efficiency.

- Short-Term Planning: Useful for making short-term production decisions due to its focus on variable costs.

Disadvantages of Marginal Cost Analysis:

- Complexity: Calculating marginal cost requires separating fixed and variable costs, which can be complex in some cases.

- Assumptions: Marginal cost analysis assumes that all variable inputs are perfect substitutes, which might not always be the case.

- Limited Focus: Marginal cost analysis often focuses on short-term decisions and variable costs, neglecting long-term fixed costs.

- Sunk Costs: Ignores sunk costs, which are past costs that cannot be recovered, leading to incomplete cost consideration.

- Varied Impact: The impact of marginal cost varies depending on the production level and industry characteristics.

- Time-Consuming: Regularly recalculating marginal cost for changing production levels can be time-consuming.

- Market Fluctuations: In dynamic markets, marginal cost might fluctuate due to changes in input costs, affecting decision-making.

- Lack of Non-Monetary Factors: Marginal cost analysis may not consider qualitative factors like quality, customer satisfaction, or long-term consequences.

- Value of Fixed Costs: The impact of marginal cost may diminish as businesses focus on fixed costs and long-term strategies.

- Marginal Revenue Variability: In some cases, marginal cost can be stable while marginal revenue fluctuates, leading to complex decisions.

Important Differences between Opportunity Cost and Marginal Cost

|

Basis of Comparison |

Opportunity Cost |

Marginal Cost |

| Definition | Value of next best alternative | Additional cost of one unit |

| Focus | Choice comparisons | Production level impact |

| Scope | General decision-making | Short-term production |

| Calculation | Comparative assessment | Incremental calculation |

| Involves | Trade-offs between alternatives | Variable cost change |

| Fixed Costs | May include fixed costs | Focuses on variable costs |

| Future Gains | Foregone potential benefits | Additional cost change |

| Decision Context | Broader decision scope | Production optimization |

| Quantification | Can include non-monetary factors | Often monetary values |

| Time Frame | Short and long-term | Primarily short-term |

| Sunk Costs | May involve sunk costs | Excludes sunk costs |

| Application | Choices involving resources | Production and pricing |

Similarities between Opportunity Cost and Marginal Cost

- Economic Concepts: Both opportunity cost and marginal cost are fundamental concepts in economics.

- Decision-Making: Both concepts play a crucial role in decision-making by providing insights into trade-offs and costs.

- Resource Allocation: They both aid in optimizing resource allocation, whether it’s about choosing alternatives or determining production levels.

- Comparative Analysis: Both involve comparing different options to assess their relative benefits and drawbacks.

- Variable Costs: Both concepts are influenced by variable costs, which change based on the quantity produced or the choice made.

- Trade–offs: Both highlight the trade-offs that individuals, businesses, and entities face when making choices.

- Maximization Objectives: Both are used to maximize certain objectives—opportunity cost maximizes benefit, while marginal cost helps maximize profit.

- Short–Term Focus: While opportunity cost can have both short and long-term implications, both concepts are often considered in short-term decision-making.

- Incremental Analysis: Both involve analyzing the impact of incremental changes, whether it’s in terms of choosing an alternative or producing one more unit.

- Mathematical Calculation: Both can be quantified and calculated, allowing for numerical comparisons and assessments.

- Decision Framework: Both provide a framework for systematically evaluating alternatives and their associated costs.

- Importance in Business: Both concepts are crucial for businesses to make informed decisions about production levels, pricing strategies, and resource allocation.

Advisory Note: Article shared based on knowledge available on internet and for the Knowledge purpose only. Please contact Professional/Advisor/Doctor for treatment/Consultation.

Articles on intactone.com are general information, and are not intended to substitute for Professional Advice. The information is “AS IS”, “WITH ALL FAULTS”. User assumes all risk of Use, Damage, or Injury. You agree that we have no liability for any damages.