by

by A debenture is a long-term debt instrument issued by a company to borrow money from the public or institutional investors. It represents a written acknowledgment of debt, specifying the principal amount, interest rate (coupon), repayment schedule, and security terms. Debenture holders are creditors of the company, not owners; they have no voting rights but receive fixed interest payments regardless of profitability. Interest is tax-deductible for the company, reducing the effective cost. Debentures may be secured (backed by company assets) or unsecured, redeemable (repaid at maturity) or irredeemable (perpetual), convertible (exchangeable for equity shares) or non-convertible. They are typically issued in denominations of ₹1,000 or ₹10,000 and traded on stock exchanges. Debentures offer regular fixed income to investors and cheaper, non-dilutive finance to companies, but they create mandatory interest obligations and financial risk.

Nature of Debentures:

1. Written Acknowledgement of Debt

Debentures are a written certificate issued by a company to acknowledge its debt. It clearly shows that the company has borrowed money from investors. The company promises to repay the principal amount after a fixed period. It also agrees to pay interest regularly. This written document acts as legal proof of borrowing. Therefore, debentures represent a formal and secure way of raising long term funds for business.

2. Fixed Rate of Interest

Debentures carry a fixed rate of interest, which is paid to debenture holders at regular intervals. This interest is paid regardless of the company’s profit or loss. It is a fixed financial obligation for the company. Investors prefer debentures because they provide stable and predictable income. Hence, fixed interest is an important feature of debentures.

3. No Ownership Rights

Debenture holders are creditors, not owners of the company. They do not have voting rights or control over management decisions. Their role is limited to receiving interest and repayment of principal. This distinguishes debentures from equity shares. Therefore, debentures do not affect the ownership structure of the company.

4. Secured or Unsecured

Debentures can be secured or unsecured. Secured debentures are backed by company assets, which can be used as security in case of default. Unsecured debentures do not have any such security and depend on the company’s creditworthiness. This nature gives companies flexibility in raising funds. It also allows investors to choose based on their risk preference.

5. Transferable Instrument

Debentures are generally transferable in the market. Investors can buy and sell them easily. This provides liquidity to debenture holders. Transferability makes debentures attractive as an investment option. It also helps in developing a secondary market for such securities. Therefore, debentures are flexible and convenient financial instruments.

6. Redeemable in Nature

Most debentures are redeemable after a fixed period. The company repays the principal amount on maturity. This gives certainty to investors about their investment period. Some debentures may also be redeemable before maturity under specific conditions. Hence, redeemability is an important aspect of debentures.

7. Priority in Repayment

In case of liquidation of the company, debenture holders are given priority over shareholders. They are repaid before equity shareholders. This reduces the risk for debenture holders. It ensures better safety of their investment. Therefore, debentures are considered safer compared to shares.

8. Long Term Source of Finance

Debentures are mainly used for raising long term funds. Companies issue them to finance expansion, modernization, or large projects. They provide stable and continuous funds over a long period. This makes them suitable for long term financial needs. Hence, debentures are an important source of long term finance.

Types of Debentures:

1. Secured Debentures (Mortgage Debentures)

Secured debentures are backed by a charge on the company’s specific assets (e.g., land, building, plant) or all assets generally. If the company defaults on interest or principal repayment, debenture holders can sell the charged assets to recover their money. The charge is created through a trust deed, and an independent trustee represents debenture holders’ interests. Secured debentures offer lower risk to investors, therefore they carry a lower interest rate compared to unsecured debentures. They are the most common type issued, especially by manufacturing companies with substantial fixed assets. The security may be fixed (specific asset named) or floating (general pool of assets like inventory and receivables). While safer for investors, secured debentures restrict the company’s freedom to sell or further mortgage those assets without debenture holders’ consent.

2. Unsecured Debentures (Naked Debentures)

Unsecured debentures, also called naked debentures, have no specific asset backing or charge on company property. Investors rely solely on the company’s general creditworthiness and reputation for repayment. In case of default, unsecured debenture holders become ordinary creditors (like trade creditors) and rank below secured creditors and statutory dues but above preference and equity shareholders in liquidation. Due to higher risk, these debentures carry a higher interest rate to attract investors. They are typically issued by well-established, highly profitable companies with excellent credit ratings and strong cash flows. Unsecured debentures offer greater flexibility to the company (no assets are tied up) but are less common because most investors demand security. They are often issued as convertible debentures to reduce investor risk perception.

3. Redeemable Debentures

Redeemable debentures are issued with a fixed maturity date on which the company must repay the principal amount to debenture holders. The repayment may be made as a lump sum (bullet repayment) or in installments over time. The company usually creates a Debenture Redemption Reserve (DRR) and may operate a sinking fund to accumulate money for repayment. Redemption can also be done through a call option (company forces early redemption) or put option (investor demands early redemption). Most debentures issued in practice are redeemable. Advantages include giving the company flexibility to reduce debt when surplus funds are available. Disadvantages include repayment pressure and the need to arrange large funds at maturity. The redemption period typically ranges from 5 to 15 years.

4. Irredeemable Debentures (Perpetual Debentures)

Irredeemable debentures, also called perpetual debentures, have no fixed maturity date. The company is not obligated to repay the principal amount during its lifetime; it only pays periodic interest forever. Repayment occurs only upon liquidation of the company or if the company voluntarily decides to redeem them (usually with a call option after a notice period). These are rare in practice because investors prefer certainty of repayment, and accounting standards (Ind AS/IFRS) often treat perpetual instruments as equity rather than debt. From the company’s perspective, perpetual debentures avoid refinancing risk and repayment pressure. However, they carry a higher interest rate than redeemable debentures to compensate investors for lack of maturity. Tax authorities may also treat perpetual interest as equity distribution in some jurisdictions.

5. Convertible Debentures

Convertible debentures give the holder the right to convert all or part of the debenture into equity shares of the company at a predetermined conversion price and within a specified conversion period. They are hybrid instruments—initially debt, potentially becoming equity. Fully convertible debentures (FCDs) convert entirely into equity on a specified date. Partly convertible debentures (PCDs) have a portion converted to equity, while the remaining portion remains as debt and is redeemed normally. Conversion is attractive to investors when the company’s share price rises above the conversion price. Convertible debentures typically carry a lower interest rate because investors get the upside potential of equity. Companies benefit by paying lower interest and delaying equity dilution. However, conversion can dilute existing shareholders’ earnings per share and control.

6. Non-Convertible Debentures (NCDs)

Non-convertible debentures (NCDs) cannot be converted into equity shares under any circumstances. They remain pure debt instruments throughout their life. The holder receives periodic interest (fixed or floating) and gets back the principal at maturity. Since there is no equity upside, NCDs must offer a higher interest rate than convertible debentures to attract investors. NCDs are popular among conservative investors seeking regular fixed income with higher safety (especially secured NCDs). Companies issue NCDs when they want to raise debt without diluting ownership or future equity. NCDs may be listed on stock exchanges, providing liquidity to investors. In India, NCDs are commonly issued by non-banking financial companies (NBFCs), housing finance companies, and corporates. They are rated by credit rating agencies (AAA, AA, etc.) indicating default risk.

7. Registered Debentures

Registered debentures are issued in the name of a specific owner, and the company maintains a register of debenture holders. Interest payments and principal repayment are made only to the person whose name appears in the register. Transfer of ownership requires a formal transfer deed and endorsement in the company’s books. This provides security to the company (knows who its creditors are) and to the investor (lost certificates can be replaced). However, transfer is slower and involves paperwork. Registered debentures are the norm today due to regulatory requirements and dematerialization (demat) in stock exchanges. Most corporate debentures issued in India and other major markets are registered with depositories (NSDL, CDSL), making transfers electronic and instant while maintaining registration.

8. Bearer Debentures

Bearer debentures are not registered in the name of any owner. Physical possession of the certificate is proof of ownership. Whoever holds the certificate is entitled to receive interest and principal—no registration needed. Transfer is as simple as handing over the certificate, requiring no paperwork or intimation to the company. Interest is paid through coupons attached to the certificate (hence “coupon rate”). Bearer debentures offer high liquidity and anonymity to investors. However, they carry high risk—lost or stolen certificates cannot be replaced, and the company has no record of who its creditors are. Due to concerns over tax evasion, money laundering, and terrorist financing, bearer debentures have been banned or severely restricted in most countries, including India. They are now largely obsolete.

9. First Debentures vs. Second Debentures (Subordination)

This classification relates to the priority of repayment during liquidation. First debentures (senior debentures) have the highest claim on the company’s assets or specific charged assets. They are repaid before any other debenture holders. Second debentures (subordinate or junior debentures) are repaid only after first debenture holders are fully satisfied. If asset value is insufficient, second debenture holders may receive partial payment or nothing. Second debentures carry higher interest rates to compensate for this additional risk. Subordination can be extended to third, fourth, etc., levels. Companies use this structure to raise multiple layers of debt at different costs—senior debt at lower cost (safer) and junior debt at higher cost. Subordinated debentures are often treated as “near-equity” by credit rating agencies and improve the company’s solvency ratios.

10. Zero-Coupon Debentures (ZCDs) / Deep Discount Bonds

Zero-coupon debentures do not pay periodic interest. Instead, they are issued at a substantial discount to their face value and redeemed at par (face value) at maturity. The difference between issue price and redemption price represents the interest (return) to the investor, which accrues over time. For example, a debenture with face value ₹1,000 may be issued at ₹600 and redeemed after 5 years at ₹1,000, giving an effective yield of approximately 10.7% per annum. ZCDs eliminate reinvestment risk (no interim coupons to reinvest) and provide known lump-sum maturity value. Companies benefit by avoiding periodic cash outflows for interest, useful when early project cash flows are negative. However, the interest is taxable as capital gains or accrued interest depending on jurisdiction. ZCDs are popular in long-term infrastructure financing.

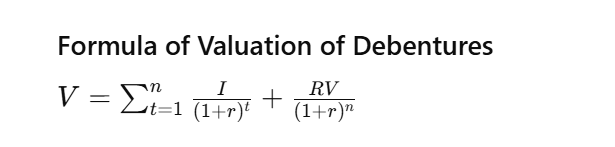

Valuation of Debentures:

Valuation of debentures means finding the present value (current worth) of a debenture based on its future cash flows. A debenture provides two types of returns:

Interest (paid regularly) and Principal (repaid at maturity).

The value of a debenture is calculated by discounting these future payments at the required rate of return.

V = Value of debenture

I = Annual interest payment

r = Required rate of return

n = Number of years

RV = Redemption value (amount repaid at maturity)

Explanation

- The first part of the formula calculates the present value of interest payments.

- The second part calculates the present value of the redemption amount.

Total of both gives the value of the debenture.

Higher required return leads to lower value of debenture.

One thought on “Debentures, Nature, Types, Valuation”