by

by Pension funds are financial institutions that collect and invest money to provide income after retirement. They are created to ensure financial security for individuals in old age. Contributions are made regularly by employees, employers, or both during the working period. These funds are invested in various assets like shares, bonds, and government securities to generate returns over time. In India, pension funds are regulated by the Pension Fund Regulatory and Development Authority. Schemes like the National Pension System help individuals build retirement savings. Pension funds promote long term investment, encourage savings habits, and reduce dependency after retirement, contributing to financial stability and economic development.

Historical Context of Pension Funds in India:

1. Early Pension System (Pre 1990s)

The pension system in India initially focused on government employees. Traditional pension schemes were based on defined benefits, where retirees received fixed income after retirement. These pensions were funded by the government and did not require employee contributions. Private sector employees had limited access to organized pension schemes and depended on savings or employer provided benefits. The system lacked uniformity and was not financially sustainable in the long run. Increasing life expectancy and rising pension liabilities created pressure on government finances. This highlighted the need for a more structured and contributory pension system in India.

2. Shift to Reforms (1990s to Early 2000s)

Economic reforms in the 1990s led to major changes in the pension system. The government recognized the need for a sustainable and transparent system. A shift began from defined benefit to defined contribution schemes, where individuals contribute towards their retirement. In 2003, a new pension system was introduced for government employees, focusing on long term savings and investment based returns. This reform aimed to reduce the financial burden on the government. It also improved efficiency and accountability. The changes marked the beginning of a modern pension framework in India.

3. Introduction of NPS and Regulation

The introduction of the National Pension System in 2004 was a major milestone. It was initially launched for government employees and later extended to all citizens. The system is regulated by the Pension Fund Regulatory and Development Authority. NPS follows a defined contribution model, where returns depend on market performance. It offers flexibility, transparency, and portability. This reform improved participation in pension savings and created a structured retirement system. It also encouraged individuals from the private sector to plan for retirement.

4. Recent Developments and Expansion

In recent years, the pension system in India has expanded significantly. The Pension Fund Regulatory and Development Authority has introduced new schemes and simplified processes to increase participation. Digital platforms have made account management easy and accessible. Awareness about retirement planning has also increased. Pension funds now play an important role in long term investment and capital formation. The system continues to evolve with better regulations and investment options. These developments aim to provide wider coverage, financial security, and a stable retirement income for all sections of society.

Objectives of Pension funds:

1. Provide Retirement Income

The main objective of pension funds is to provide regular income after retirement. Individuals contribute during their working years so they can receive financial support later in life. This ensures stability when earning capacity reduces. Pension funds help maintain a standard of living even after retirement. They reduce dependence on family or external support. In India, schemes regulated by the Pension Fund Regulatory and Development Authority aim to ensure steady income for retirees. This objective is important for financial security and dignity in old age.

2. Encourage Long Term Savings

Pension funds promote the habit of saving money regularly over a long period. Individuals contribute small amounts consistently, which grow over time through investments. This helps build a strong financial base for the future. Long term savings also create financial discipline among individuals. It ensures that people prepare early for retirement needs. Pension schemes encourage systematic investment rather than irregular saving. By promoting long term savings, pension funds support financial planning and stability. This objective also helps in creating a savings culture in the economy.

3. Ensure Financial Security

Pension funds aim to provide financial security during old age. They protect individuals from financial difficulties after retirement when income sources are limited. By building a retirement corpus, pension funds reduce uncertainty and risk. This security helps individuals manage daily expenses, healthcare, and other needs. It also provides peace of mind and independence. The Pension Fund Regulatory and Development Authority ensures that pension funds operate safely and transparently. Financial security is a key objective that improves quality of life after retirement.

4. Reduce Dependency

Pension funds help individuals become financially independent in their later years. Without proper savings, retired individuals may depend on family members or government support. Pension income reduces this dependency and promotes self reliance. It allows individuals to manage their own expenses and maintain dignity. This objective is important in a country like India where social security systems are still developing. By ensuring independent income after retirement, pension funds improve personal and social well being. They also reduce the burden on families and society.

5. Promote Capital Formation

Pension funds contribute to capital formation in the economy. The collected funds are invested in various financial instruments like bonds, shares, and government securities. These investments support business growth and infrastructure development. Long term funds from pension schemes are stable and reliable sources of finance. This helps in economic development and job creation. By channelizing savings into productive investments, pension funds strengthen the financial system. This objective benefits both individuals and the overall economy.

6. Provide Investment Growth

Pension funds aim to grow the invested money over time. Contributions are invested in diversified assets to earn returns. Professional fund managers handle these investments to maximize gains and reduce risk. Over a long period, compounding helps in increasing the value of the fund. This growth ensures that individuals receive adequate funds after retirement. The Pension Fund Regulatory and Development Authority monitors investment practices to ensure safety and transparency. Investment growth is essential for building a strong retirement corpus.

7. Support Social Security

Pension funds play an important role in strengthening social security systems. They provide financial support to individuals in old age, reducing poverty among elderly people. In countries like India, pension schemes complement government welfare programs. They ensure that retired individuals can meet their basic needs without hardship. By improving financial stability, pension funds contribute to social welfare and economic balance. This objective helps in building a secure and stable society.

8. Encourage Retirement Planning

Pension funds encourage individuals to plan for their future early in life. They create awareness about the importance of retirement savings. Proper planning helps individuals set financial goals and invest accordingly. Pension schemes provide structured options for systematic investment. This reduces financial stress in later years. With guidance from regulators like the Pension Fund Regulatory and Development Authority, individuals can make informed decisions. Encouraging retirement planning ensures better financial management and a secure future.

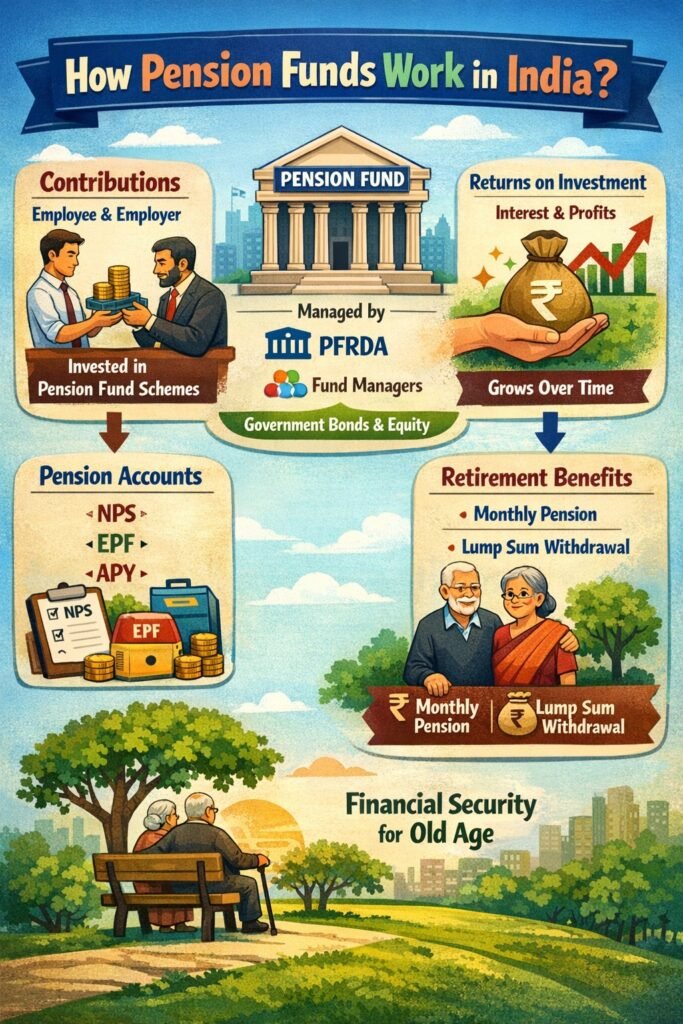

How does Pension Funds work in India?

1. Contribution and Account Opening

Pension funds in India start with opening an account under schemes like the National Pension System. Individuals, employees, or employers make regular contributions during the working period. Contributions can be monthly or yearly, depending on the plan. These payments form the basic retirement savings. The system is regulated by the Pension Fund Regulatory and Development Authority to ensure safety and transparency. Early and consistent contributions help in building a large retirement corpus. This step creates financial discipline and encourages long term planning for retirement needs.

2. Investment of Funds

After collection, the contributions are invested in different financial instruments. Professional fund managers allocate money into equities, corporate bonds, and government securities based on risk preference. Diversification helps in reducing risk and improving returns. The Pension Fund Regulatory and Development Authority sets guidelines for safe investment practices. Individuals may choose their investment option depending on their risk level. These investments generate income over time. Proper management ensures that funds grow steadily and are protected from major losses. This stage is important for increasing the value of retirement savings.

3. Growth through Compounding

Pension funds grow over time due to the power of compounding. Returns earned on investments are reinvested, leading to higher earnings in the future. The longer the investment period, the greater the growth. Regular contributions combined with compounding create a strong retirement corpus. Even small amounts can grow significantly over time. The Pension Fund Regulatory and Development Authority ensures that fund managers follow proper practices to maintain steady growth. This stage highlights the importance of starting early and staying invested for long term financial security.

4. Withdrawal and Annuity

At the time of retirement, the accumulated pension fund can be used in two ways. A portion can be withdrawn as a lump sum, while the remaining amount is used to buy an annuity. Annuity provides regular income after retirement, ensuring financial stability. The Pension Fund Regulatory and Development Authority regulates this process to protect subscribers. The income received depends on the total savings and annuity plan chosen. This stage ensures continuous financial support and helps individuals maintain their standard of living after retirement.

Types of Pension funds in India:

1. Government Pension Funds

Government pension funds are meant for employees working in central and state governments. Earlier, these were defined benefit schemes where retirees received fixed pensions funded by the government. Now, most new employees are covered under contributory schemes like the National Pension System. Contributions are made by both employee and government. These funds are regulated by the Pension Fund Regulatory and Development Authority. They ensure financial security after retirement. Government pension funds are reliable and structured, providing steady income and long term stability for public sector employees.

2. Employee Pension Schemes (EPS)

Employee Pension Scheme is a social security scheme for organized sector workers. It is managed by the Employees’ Provident Fund Organisation. Under this scheme, a portion of the employer’s contribution to the provident fund is allocated to pension. Employees become eligible for pension after completing a minimum number of service years. The scheme provides monthly pension after retirement, disability, or to family members in case of death. EPS ensures financial support for workers in their old age. It plays an important role in providing social security and reducing financial risk for salaried employees.

3. National Pension System (NPS)

The National Pension System is a voluntary and contributory pension scheme open to all citizens. It is regulated by the Pension Fund Regulatory and Development Authority. Individuals contribute regularly and choose investment options based on risk preference. Funds are invested in equities, bonds, and government securities. At retirement, a portion can be withdrawn, and the rest is used to buy annuity for regular income. NPS is flexible, portable, and transparent. It encourages long term savings and is widely used by both government and private sector employees.

4. Public Provident Fund (PPF)

The Public Provident Fund is a long term savings scheme that also serves as a retirement fund. It is backed by the government and offers safe and guaranteed returns. Individuals can invest regularly with a fixed tenure. Interest earned is tax free, making it attractive for long term savings. Although not a direct pension scheme, it helps in building a retirement corpus. PPF is suitable for risk averse investors who prefer safety over high returns. It promotes disciplined saving and provides financial security in the long run.

5. Private Pension Funds

Private pension funds are offered by insurance companies and financial institutions. These funds provide retirement plans where individuals invest regularly to build a pension corpus. At maturity, they receive lump sum and regular income through annuity. These funds are regulated by the Insurance Regulatory and Development Authority of India. They offer different plans based on risk and return preferences. Private pension funds provide flexibility and additional options beyond government schemes. They help individuals plan retirement according to their financial goals and ensure financial security after retirement.

| Scheme | Who Can Join | Contributions | Benefits |

|---|---|---|---|

| EPF (Employees’ Provident Fund) | Salaried employees | Employee + Employer | Lump sum + interest at retirement |

| GPF (General Provident Fund) | Govt. employees | Employee only | Lump sum + guaranteed interest |

| NPS (National Pension System) | Open to all citizens | Flexible (employee/self) | Monthly pension + lump sum; tax benefits |

| APY (Atal Pension Yojana) | Unorganized sector | Fixed monthly contribution | Guaranteed pension ₹1,000–₹5,000/month |

Regulators of Pension funds in India:

1. Pension Fund Regulatory and Development Authority (PFRDA)

The Pension Fund Regulatory and Development Authority is the main regulator of pension funds in India. It was established to develop and regulate the pension sector and ensure retirement security for citizens. PFRDA supervises schemes like the National Pension System and Atal Pension Yojana. It sets rules for registration, functioning, and investment of pension funds. The authority ensures transparency, safety, and fair practices. It also protects the interests of subscribers by monitoring fund managers and intermediaries. By promoting awareness and expanding pension coverage, PFRDA plays a key role in strengthening the pension system in India.

2. Reserve Bank of India (RBI)

The Reserve Bank of India plays an indirect but important role in regulating pension funds in India. It controls monetary policy and financial stability, which affect pension fund investments. RBI regulates banks and financial institutions where pension funds are invested or managed. It also supervises payment systems used for pension transactions. Through its policies on interest rates and liquidity, RBI influences returns on pension investments. Although it does not directly manage pension schemes, its role is crucial in maintaining a stable financial environment for safe and efficient functioning of pension funds.

3. Securities and Exchange Board of India (SEBI)

The Securities and Exchange Board of India regulates the capital markets where pension funds invest a portion of their money. It ensures transparency, fair trading, and investor protection in stock markets and mutual funds. Pension funds investing in equities and securities must follow SEBI guidelines. This reduces risk and ensures proper disclosure of information. SEBI also monitors intermediaries like brokers and asset management companies. Its role helps in maintaining trust and efficiency in the financial markets. This indirectly supports the growth and safety of pension fund investments.

4. Insurance Regulatory and Development Authority of India (IRDAI)

The Insurance Regulatory and Development Authority of India regulates insurance companies that provide annuity plans and pension products. After retirement, pension funds are often used to purchase annuities, which provide regular income. IRDAI ensures that insurance companies follow fair practices and protect policyholders. It sets rules for pricing, claims, and service standards. This helps in ensuring reliable and timely pension payments. IRDAI also promotes growth of pension related insurance products. Its role is important in maintaining trust and stability in the retirement income system.

Challenges of Pension funds in India:

1. Low Pension Coverage

A major challenge in India is limited pension coverage, especially in the unorganized sector. A large portion of the workforce does not have access to formal pension schemes. Lack of awareness, irregular income, and absence of employer support reduce participation. Even though schemes regulated by the Pension Fund Regulatory and Development Authority are available, many people remain outside the system. This leads to financial insecurity after retirement. Expanding coverage and improving accessibility is essential to ensure that more people benefit from pension funds and achieve long term financial stability.

2. Lack of Awareness and Financial Literacy

Many individuals in India are not aware of pension schemes or their benefits. Limited financial literacy makes it difficult for people to understand long term retirement planning. As a result, they delay or avoid investing in pension funds. Misconceptions about low returns and long lock in periods also reduce interest. Although efforts are made by the Pension Fund Regulatory and Development Authority, awareness levels remain low. Increasing education through campaigns and simple guidance is necessary. Better awareness will help individuals make informed decisions and improve participation in pension schemes.

3. Market Risk and Uncertain Returns

Pension funds invest in financial markets, which are subject to fluctuations. Changes in interest rates, inflation, and stock market conditions affect returns. This creates uncertainty in the final pension amount. Unlike traditional schemes, returns are not guaranteed in market linked plans. This risk may discourage conservative investors. Although diversification helps reduce risk, it cannot eliminate it completely. The Pension Fund Regulatory and Development Authority provides guidelines for safe investment, but uncertainty remains. Managing risk while ensuring stable returns is a major challenge for pension funds in India.

4. Inflation Risk

Inflation reduces the purchasing power of money over time. Even if individuals receive pension income, rising prices may make it insufficient to meet future expenses. This is a major concern for long term retirement planning. Pension funds must generate returns higher than inflation to maintain real value. However, achieving this consistently is difficult. Many people underestimate the impact of inflation while planning for retirement. Although regulators like the Pension Fund Regulatory and Development Authority encourage proper investment strategies, inflation risk remains a key challenge in ensuring adequate retirement income.

5. Limited Contribution Capacity

Many individuals, especially in low income groups, are unable to contribute regularly to pension funds. Irregular earnings and financial constraints reduce their ability to save for retirement. This leads to a smaller pension corpus and lower income after retirement. Even when schemes are available, affordability becomes a barrier. The Pension Fund Regulatory and Development Authority promotes flexible contribution options, but participation is still affected. Increasing income levels and providing incentives can help improve contributions. Addressing this issue is important for building a strong and inclusive pension system.

6. Regulatory and Operational Challenges

Managing pension funds involves strict rules and continuous monitoring. Compliance with regulations set by the Pension Fund Regulatory and Development Authority increases operational complexity and costs. Frequent changes in policies require adjustments by fund managers and institutions. Ensuring transparency and accountability across all participants is challenging. Coordination between different regulators and institutions is also required. While regulation is necessary for safety, excessive control may slow growth. Balancing regulation with flexibility is important to improve efficiency and development of pension funds in India.

7. Longevity Risk

Longevity risk refers to the possibility of individuals living longer than expected. This increases the need for sustained pension income over a longer period. If the pension corpus is not sufficient, individuals may face financial difficulties in later years. With improving healthcare, life expectancy in India is rising, making this challenge more significant. Pension funds must plan for long term payouts, which requires careful investment and management. The Pension Fund Regulatory and Development Authority oversees such risks, but ensuring adequate funds for longer life spans remains a major concern.