by

by Scarcity, refers to the basic fact of life that there exists only a finite amount of human and nonhuman resources which the best technical knowledge is capable of using to produce only limited maximum amounts of each economic good. If the conditions of scarcity didn’t exist and an infinite amount of every good could be produced or human wants fully satisfied there would be no economic goods, i.e. goods that are relatively scarce. Scarcity is the limited availability of a commodity, which may be in demand in the market or by the commons. Scarcity also includes an individual’s lack of resources to buy commodities. The opposite of scarcity is abundance.

Scarcity plays a key role in economic theory, and it is essential for a “proper definition of economics itself.”

Scarcity refers to a limited supply of goods. That scarcity can then lead to high demand from consumers. According to the scarcity principle, the price of an item in low supply and high demand will steadily rise to meet the consumers’ expected demand. As a result, businesses may use this economic theory to achieve higher profits. If businesses create a sense of scarcity for a product, it can make consumers more eager to purchase it because they worry they may not have the opportunity to buy it in the future.

This economic theory also aligns with the concept of market equilibrium. Market equilibrium represents when supply equals demand. However, market demands and supplies change constantly, so they cannot always be in equilibrium. For example, if the market price of a good falls, its manufacturers may produce less of that good because the price does not cover their production costs. Producing less of that good results in scarcity for the consumers, thus driving its price in the market toward the equilibrium price to meet demand.

“The best example is perhaps Walras’ definition of social wealth, i.e., economic goods. ‘By social wealth’, says Walras, ‘I mean all things, material or immaterial (it does not matter which in this context), that are scarce, that is to say, on the one hand, useful to us and, on the other hand, only available to us in limited quantity’.”

British economist Lionel Robbins is famous for his definition of economics which uses scarcity

“Economics is the science which studies human behaviour as a relationship between ends and scarce means which have alternative uses.”

Economic theory views absolute and relative scarcity as distinct concepts and is “quick in emphasizing that it is relative scarcity that defines economics. “Current economic theory is derived in large part from the concept of relative scarcity which “states that goods are scarce because there are not enough resources to produce all the goods that people want to consume”.

There are three main causes of scarcity in the economy:

Demand scarcity: When there is a high demand for a resource or product, due to increasing populations or changes in preferences.

Supply scarcity: When the supply or resource is low or out, due to weather, disasters or resource depletion.

Structural scarcity: When there is mismanagement or inequality of access to populations, often because of politics or location.

Malthus and Absolute Scarcity

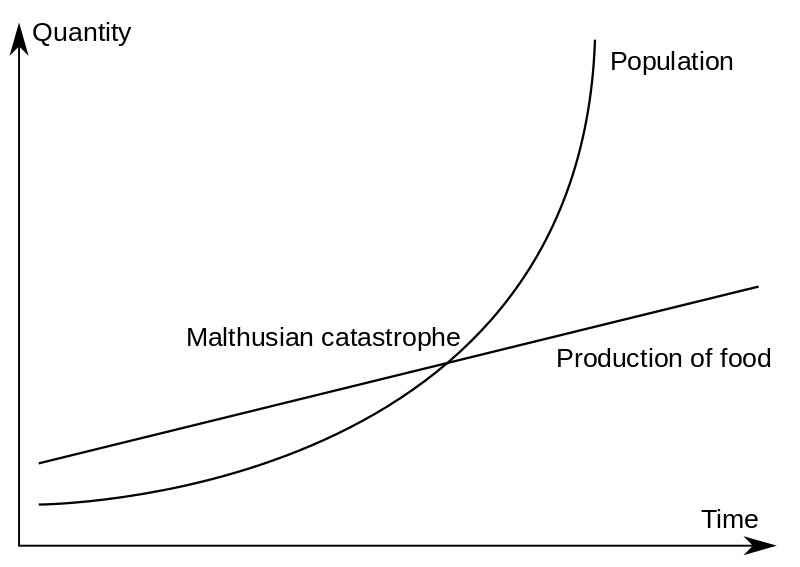

Malthus observed that an increase in a nation’s food production improved the well-being of the populace, but the improvement was temporary because it led to population growth, which in turn restored the original per capita production level. In other words, humans had a propensity to utilize abundance for population growth rather than for maintaining a high standard of living, a view that has become known as the “Malthusian trap” or the “Malthusian spectre”. Populations had a tendency to grow until the lower class suffered hardship, want and greater susceptibility to famine and disease, a view that is sometimes referred to as a Malthusian catastrophe. Malthus wrote in opposition to the popular view in 18th-century Europe that saw society as improving and in principle as perfectible.

Schematic of the Malthusian catastrophe

Malthusianism is the idea that population growth is potentially exponential while the growth of the food supply or other resources is linear, which eventually reduces living standards to the point of triggering a population die off. It derives from the political and economic thought of the Malthus, as laid out in his 1798 writings, An Essay on the Principle of Population. Malthus believed there were two types of ever-present “checks” that are continuously at work, limiting population growth based on food supply at any given time:

- Preventive checks, such as moral restraints or legislative action; for example the choice by a private citizen to engage in abstinence and delay marriage until their finances become balanced, or restriction of legal marriage or parenting rights for persons deemed “Deficient” or “unfit” by the government.

- Positive checks, such as disease, starvation, and war, which lead to high rates of premature death resulting in what is termed a malthusian catastrophe. The adjacent diagram depicts the abstract point at which such an event would occur, in terms of the existing population and food supply: when the population reaches or exceeds the capacity of the shared supply, positive checks are forced to occur, restoring balance. (in reality, the situation would be significantly more nuanced due to complex regional and individual disparities around access to food, water, and other resources.) positive checks by their nature are more “extreme and involuntary by nature”.

There are two types of scarcity implicit in Malthusianism, namely scarcity of foods or “requirements” and objects that provide direct satisfaction of these food needs or “Available quantities”. These are absolute in nature and define economic concepts of scarcity, abundance, and sufficiency as follows:

- Absolute sufficiency is the condition where human requirements in the way of food needs and available quantities of useful goods are equal.

- Absolute scarcity is the condition where human requirements in the way of food needs are greater than the available quantities of useful goods.

- Absolute abundance is the condition where the available quantities of useful goods are greater than human requirements in the way of food needs.

Robbins and Relative Scarcity

Lionel Robbins was prominent member of the economics department at the London School of Economics. He is famous for the quote, “Humans want what they can’t have.” Robbins is noted as a free market economist, and for his definition of economics. The definition appears in the Essay by Robbins as:

“Economics is the science which studies human behaviour as a relationship between ends and scarce means which have alternative uses.”

Robbins found that four conditions were necessary to support this definition:

- The decision-maker wants both more income and more income-earning assets.

- The decision-maker does not have the means to choose both. In this case, the means are not identified.

- The decision-maker can “augment” (Robbins) both their income and income-earning assets. In this case, implicitly, this is a limited ability, or the project stakeholder would not be subject to scarcity.

- The decision maker’s desire for various constituent elements of income and income-earning assets are different. Robbins crucially makes the point later in his essay that this fourth condition can be restated as being “capable of being distinguished in order of importance, then behavior necessarily assumes the form of choice. “Robbins argued that there had to be a hierarchy of needs to support these conditions.

There are relative in nature and define economic concepts of scarcity, abundance, and sufficiency as follows:

- Relative sufficiency is the condition where multiple, different human requirements and available quantities with alternative uses are equal.

- Relative scarcity is the condition where multiple, different human requirements are greater than the available quantities with alternative uses.

- Relative abundance is the condition where the available quantities of useful goods with alternative uses are greater than the multiple, different human requirements.

Samuelson and Relative Scarcity

Samuelson tied the notion of relative scarcity to that of economic goods when he observed that if the conditions of scarcity didn’t exist and an “infinite amount of every good could be produced or human wants fully satisfied … there would be no economic goods, i.e. goods that are relatively scarce.” The basic economic fact is that this “limitation of the total resources capable of producing different (goods) makes necessary a choice between relatively scarce commodities.”

Modern concepts of scarcity

Scarcity refers to a gap between limited resources and theoretically limitless wants. The notion of scarcity is that there is never enough (of something) to satisfy all conceivable human wants, even at advanced states of human technology. Scarcity involves making a sacrifice giving something up, or making a trade-off in order to obtain more of the scarce resource that is wanted.

The condition of scarcity in the real world necessitates competition for scarce resources, and competition occurs “when people strive to meet the criteria that are being used to determine who gets what”. The price systems, or market prices, are one way to allocate scarce resources. “If a society coordinates economic plans on the basis of willingness to pay money, members of that society will [strive to compete] to make money”. If other criteria are used, we would expect to see competition in terms of those other criteria.