by

by Capital is essential for establishing and operating a business. Entrepreneurs require funds to purchase machinery, raw materials, buildings, and other resources necessary for production and business activities. The funds used in a business are known as capital, and they can be obtained from different sources. Understanding the sources of capital helps entrepreneurs select the most suitable financing option according to the nature and needs of the business.

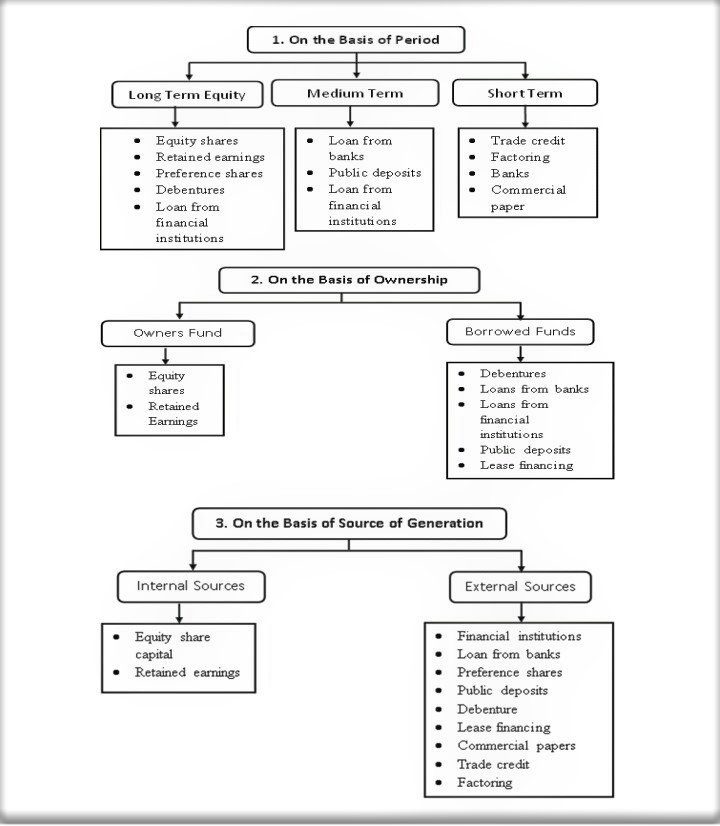

Sources of capital can be broadly classified on the basis of period, ownership, and source of generation. This classification explains the duration of funds, the ownership of capital, and the origin of funds used in business operations. Each type of capital plays a unique role in financing business activities and supporting the growth of enterprises.

1. Sources of Capital on the Basis of Period

On the basis of period, capital is classified according to the length of time for which funds are required in a business. Businesses need funds for different durations depending on their operational and investment requirements. Capital based on period is divided into short-term, medium-term, and long-term capital.

- Short-Term Capital

Short-term capital refers to funds required for a short period, usually up to one year. It is mainly used to meet the day-to-day operational needs of the business. These needs include purchasing raw materials, paying wages and salaries, meeting transportation costs, and handling other routine expenses. Short-term capital helps maintain smooth operations and ensures that the business can continue its activities without interruption.

Short-term capital is generally obtained from sources such as trade credit, bank overdrafts, short-term bank loans, advances from customers, and credit purchases from suppliers. These sources provide quick financial support and help businesses manage temporary financial shortages.

Example: A small garment manufacturing unit may require funds to purchase fabric and pay workers for the production of clothing. The entrepreneur may obtain trade credit from suppliers, allowing payment to be made after 30 or 60 days. This arrangement provides short-term capital to maintain production without immediate cash payment.

Short-term capital is important because it helps businesses manage working capital and maintain liquidity. However, it must be carefully managed to avoid excessive borrowing or financial pressure.

- Medium-Term Capital

Medium-term capital refers to funds required for a period ranging from one to five years. It is used for investments that are not purely short-term but also do not require very long-term financing. Businesses often use medium-term capital for purchasing machinery, vehicles, office equipment, or for expanding production capacity.

Common sources of medium-term capital include bank loans, hire purchase agreements, leasing arrangements, and loans from financial institutions. These financing options allow businesses to acquire necessary assets and repay the borrowed amount over a moderate period.

Example: A transportation startup may need to purchase delivery vehicles to provide logistics services. Instead of paying the entire cost at once, the entrepreneur may obtain a bank loan repayable over three to five years. This loan becomes a source of medium-term capital for the business.

Medium-term capital helps businesses invest in essential assets and improve operational efficiency without creating excessive long-term financial obligations.

- Long-Term Capital

Long-term capital refers to funds required for a long period, usually more than five years. It is used for major investments such as purchasing land, constructing buildings, installing large machinery, and establishing new business units. Long-term capital supports the long-term growth and expansion of the organization.

Sources of long-term capital include equity shares, preference shares, debentures, venture capital, retained earnings, and long-term bank loans. These sources provide substantial financial support for large-scale investments.

Example: A technology startup planning to build a large manufacturing facility for electronic devices may require a significant amount of capital. The entrepreneur may raise funds by issuing equity shares or obtaining investment from venture capitalists. This investment provides long-term capital for establishing the facility.

Long-term capital provides stability to businesses and allows them to undertake large development projects that support future growth.

2. Sources of Capital on the Basis of Ownership

On the basis of ownership, capital is classified according to who owns the funds invested in the business. This classification includes owned capital and borrowed capital.

- Owned Capital

Owned capital refers to funds that belong to the owners of the business. These funds are invested by entrepreneurs or shareholders and represent their ownership in the organization. Owned capital does not need to be repaid within a fixed period, and it forms the permanent capital of the business.

Examples of owned capital include personal savings of the entrepreneur, equity shares, retained earnings, and contributions from business partners. Since the owners provide these funds, they bear the risk of business failure but also receive the profits generated by the business.

Example: An entrepreneur starting a small restaurant may invest personal savings to purchase kitchen equipment, furniture, and initial inventory. This investment represents owned capital because it belongs to the entrepreneur.

Owned capital strengthens the financial position of the business and increases its credibility. However, entrepreneurs may sometimes find it difficult to raise large amounts of owned capital without external investors.

- Borrowed Capital

Borrowed capital refers to funds borrowed from external sources with an obligation to repay the principal amount along with interest. Businesses obtain borrowed capital when owned funds are insufficient to meet financial requirements.

Sources of borrowed capital include bank loans, debentures, loans from financial institutions, public deposits, and trade credit. Borrowed capital provides additional funds without requiring the entrepreneur to give up ownership of the business.

Example: A manufacturing company may take a bank loan to purchase new machinery. The company must repay the loan over a specified period along with interest. This loan represents borrowed capital.

Borrowed capital helps businesses expand operations and invest in growth opportunities. However, excessive borrowing may increase financial risk and create repayment pressure.

3. Sources of Capital on the Basis of Source of Generation

On the basis of source of generation, capital is classified according to where the funds originate from. This classification includes internal sources and external sources of capital.

- Internal Sources of Capital

Internal sources of capital refer to funds generated within the business organization. These funds are usually derived from the company’s own operations and resources.

Examples of internal sources include retained earnings, depreciation funds, sale of surplus assets, and reserves. Retained earnings represent profits that are reinvested in the business instead of being distributed to owners or shareholders.

Example: A successful retail business may generate profits each year. Instead of distributing all profits to the owners, a portion may be reinvested to open new branches. This reinvested profit becomes an internal source of capital.

Internal financing reduces dependence on external lenders and avoids interest payments or ownership dilution. However, it may not provide sufficient funds for large expansion projects.

- External Sources of Capital

External sources of capital refer to funds obtained from outside the organization. Businesses often rely on external financing when internal resources are insufficient for expansion or development.

Examples of external sources include bank loans, venture capital, angel investors, public deposits, government grants, and financial institution loans. These sources provide additional funds required for growth and innovation.

Example: A startup developing a mobile application may attract investment from angel investors who believe in the potential of the business idea. These investors provide funds in exchange for equity in the company. This investment represents an external source of capital.

External financing allows businesses to raise large amounts of capital and accelerate growth. However, it may involve interest payments, sharing ownership, or meeting strict financial requirements.

Factors Affecting the Choice of the Source of Funds

- Cost of Capital

The cost of capital is one of the most important factors in choosing a source of funds. Different sources of finance involve different costs such as interest, dividends, or service charges. Entrepreneurs prefer sources of finance that have lower cost so that the business can maintain higher profitability. If the cost of borrowing is too high, it may increase financial burden on the business. Therefore, entrepreneurs carefully compare the cost of different sources before selecting the most suitable option for financing their venture.

- Risk Involved

Risk is another important factor affecting the choice of funds. Some sources of finance involve higher financial risk, especially borrowed funds that require fixed interest payments. If the business fails to generate enough income, repayment may become difficult. On the other hand, owned capital does not require regular repayment and therefore carries less financial risk. Entrepreneurs must evaluate the level of risk associated with each financing option before making a decision. Proper risk assessment helps maintain financial stability and protects the business from financial difficulties.

- Control over the Business

Control over the business is a key factor while choosing a source of funds. Some sources of finance, such as equity shares or venture capital, may require entrepreneurs to share ownership and decision-making power with investors. Many entrepreneurs prefer financing methods that allow them to retain full control over business operations. Borrowed capital such as bank loans does not usually involve ownership sharing. Therefore, entrepreneurs must consider how a particular source of finance may affect their authority and control over the business.

- Purpose of Finance

The purpose for which funds are required also influences the choice of financing sources. Businesses need funds for different purposes such as working capital, purchasing machinery, expansion, or research and development. Short-term needs are usually financed through short-term sources such as trade credit or bank overdrafts. Long-term investments require long-term financing such as equity capital or long-term loans. Choosing the right source according to the purpose ensures proper utilization of funds and efficient financial management.

- Flexibility of the Source

Flexibility refers to the ease with which funds can be obtained, repaid, or adjusted according to business needs. Some sources of finance offer flexible repayment terms and conditions, which make them more attractive to entrepreneurs. For example, trade credit allows businesses to delay payment for a certain period. Flexible sources of finance help entrepreneurs manage cash flow more effectively. Businesses usually prefer financing options that provide convenience and adaptability in changing financial situations.

- Availability of Funds

Availability of funds is another factor affecting the choice of finance. Some sources of finance may not always be easily available to entrepreneurs, especially for new ventures with limited credit history. Financial institutions may require detailed documentation, collateral, or proof of business performance. Entrepreneurs must select sources that are accessible and suitable for their financial situation. The availability of funds also depends on the size and reputation of the business in the market.

- Business Stability and Profitability

The financial stability and profitability of a business influence the choice of funding sources. Businesses with stable income and strong financial performance can easily obtain loans from banks and financial institutions. On the other hand, startups or businesses with uncertain income may find it difficult to secure borrowed funds. In such cases, entrepreneurs may rely more on owned capital or investors. Therefore, the financial condition of the business plays an important role in determining suitable financing options.

- Legal and Regulatory Requirements

Legal and regulatory requirements also affect the choice of financing sources. Certain forms of finance may involve complex legal procedures, government approvals, and regulatory compliance. For example, issuing shares or raising funds from the public requires compliance with various legal regulations. Entrepreneurs must consider these requirements before selecting a source of funds. Choosing financing options that follow legal guidelines ensures transparency and protects the business from legal complications.

One thought on “Sources of Capital”