by

by Porter’s Five Forces is a strategic framework analyzing the competitive intensity and profit attractiveness of an industry. It moves beyond traditional competitor-focused analysis to examine five structural forces that shape industry competition.

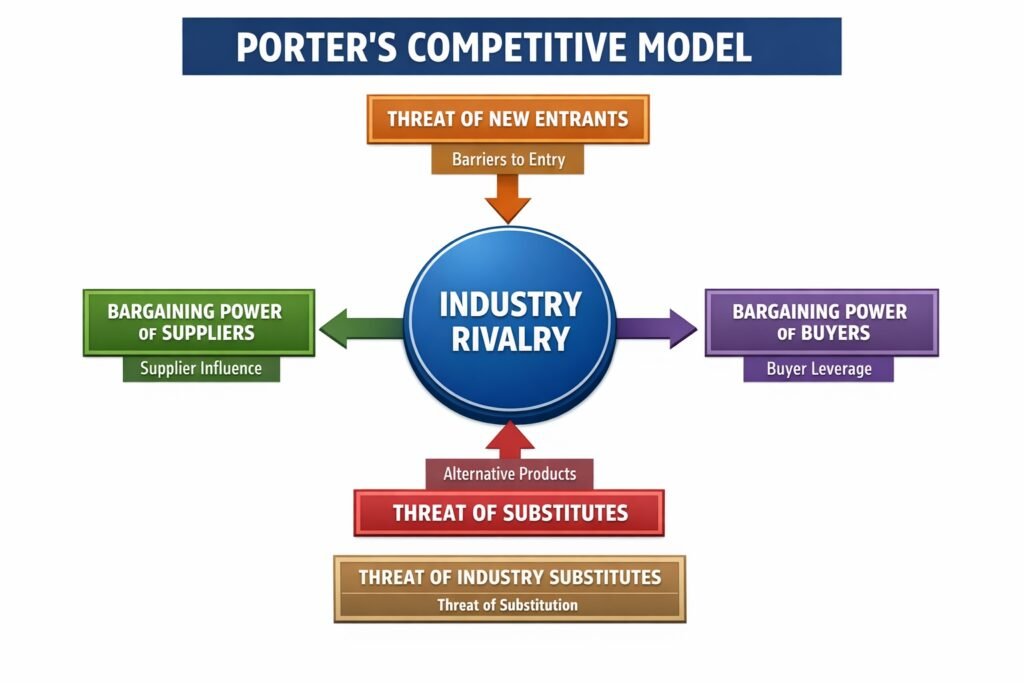

Functions of Porter’s Competitive Model:

1. Industry Analysis

Porter’s Competitive Model helps in analyzing the structure of an industry. It examines factors such as competition, entry barriers, supplier power, buyer power, and substitutes. This analysis gives a clear understanding of how the industry operates. It helps managers identify the level of competition and profitability. By studying these forces, organizations can understand the intensity of rivalry and market conditions. This function supports strategic planning and helps firms position themselves effectively. Overall, it provides a systematic approach to evaluate industry attractiveness and guides decision making.

2. Identifying Competitive Forces

The model identifies five key forces that influence competition in the market. These include threat of new entrants, bargaining power of buyers, bargaining power of suppliers, threat of substitutes, and competitive rivalry. Understanding these forces helps businesses recognize external pressures affecting performance. It enables firms to take proactive steps to manage these forces. This function helps in building strong strategies to deal with competition. Overall, it improves awareness of the competitive environment and supports better business decisions.

3. Strategy Formulation

Porter’s model supports the formulation of effective business strategies. By understanding industry forces, managers can develop strategies to gain competitive advantage. It helps in choosing the right positioning such as cost leadership or differentiation. The model guides firms in reducing threats and strengthening their market position. It also helps in selecting target markets and planning long term actions. Overall, this function ensures that strategies are based on proper analysis and are aligned with the competitive environment.

4. Risk Assessment

The model helps in identifying potential risks in the industry. By analyzing competitive forces, organizations can understand possible threats such as new competitors, substitute products, or changes in supplier power. This helps in preparing for uncertainties and reducing business risks. It supports better planning and decision making. Firms can take preventive measures to minimize negative impacts. Overall, this function improves the ability of organizations to handle risks and maintain stability in a competitive market.

5. Enhancing Competitive Advantage

Porter’s Competitive Model helps organizations build and sustain competitive advantage. By understanding industry dynamics, firms can focus on their strengths and improve performance. It allows businesses to differentiate their products or reduce costs. This leads to better customer satisfaction and market position. The model also helps in identifying opportunities for growth. Overall, it supports long term success by improving competitiveness and ensuring effective use of resources in a challenging business environment.

Components of Porter’s Competitive Model:

1. Threat of New Entrants

This component examines how easily new competitors can enter an industry and erode incumbent profits. When entry barriers are low, new firms enter freely, increasing capacity, reducing prices, and compressing margins. Entry barriers include: economies of scale (new entrants must enter at large scale or accept cost disadvantage), product differentiation (established brand loyalty requires expensive advertising to overcome), capital requirements (investment needed for plant, inventory, receivables), switching costs (one-time costs customers incur changing suppliers), access to distribution channels (existing relationships block new entrants), and government policies (licensing, patents, regulations). Industries with high barriers (aerospace, telecommunications) sustain above-average profitability; low-barrier industries (retail, restaurants) remain perennially competitive. Strategic responses include building barriers (scale investment, brand advertising) or accepting constant entry pressure and competing on operational excellence.

2. Bargaining Power of Suppliers

Supplier power measures leverage that input providers have over industry participants. Powerful suppliers can raise prices, reduce quality, shift costs, or capture industry profits. Supplier power increases when: few suppliers dominate the market (concentration exceeds buyer concentration), no substitute inputs exist, industry firms are fragmented (many buyers with no individual bargaining clout), switching costs are high (retooling for alternative inputs is expensive), suppliers can integrate forward (become competitors), or the industry is not an important customer to suppliers (suppliers indifferent to losing business). For example, Intel’s power over PC manufacturers stems from unique microprocessor technology, brand recognition, and forward integration capability. Mitigating strategies include backward integration (making inputs internally), supplier diversification (multiple sources), long-term contracting, or developing substitute inputs.

3. Bargaining Power of Buyers

Buyer power measures customers’ ability to force price reductions, demand better quality or service, or pit competitors against each other. Powerful buyers capture industry profits by extracting concessions. Buyer power increases when: few large buyers exist (buyer concentration exceeds seller concentration), products are standardized undifferentiated, buyers face low switching costs, buyers can integrate backward (produce inputs themselves), buyers are price-sensitive (product represents significant portion of their costs), or buyers have full information about supplier costs and margins. Walmart exemplifies buyer power over consumer goods suppliers. Industries serving fragmented buyer populations (individual consumers) face less pressure. Strategic responses include differentiating products (reducing buyer price sensitivity), targeting buyers with low price sensitivity, forward integration (selling directly to end-users), or selective contracting (refusing most demanding customers).

4. Threat of Substitute Products

Substitutes are products or services from outside the industry that fulfill the same customer need. Substitutes create price ceilings: if industry prices rise above substitute alternatives, customers switch. The threat depends on: substitutes’ price-performance trade-off relative to industry products (better/cheaper substitutes increase threat), buyers’ switching costs (low costs increase threat), and buyers’ propensity to substitute (willingness to accept functional equivalence). Video conferencing substitutes for business travel; streaming substitutes for cable television; generic drugs substitute for branded pharmaceuticals. Substitutes often come from seemingly unrelated industries, making them easy to overlook in traditional competitor analysis. Strategic responses include: improving product performance (raising price-performance frontier), reducing price (eliminating substitute advantage), increasing switching costs (loyalty programs, proprietary formats), or creating complementors (products that make substitutes less attractive).

5. Intensity of Rivalry Among Existing Competitors

Rivalry intensity determines how aggressively current industry participants compete for market share. High rivalry erodes profits through price wars, advertising battles, innovation races, or service competitions. Rivalry increases when: competitors are numerous or roughly equal in size (no clear leader to stabilize market), industry growth is slow (market share gains require taking from rivals), fixed costs are high (pressure to discount to cover overhead), products are perishable or undifferentiated (excess capacity leads to price cutting), exit barriers are high (firms cannot leave despite poor returns), and competitors are diverse in strategy, origin, or personality. Airlines exemplify intense rivalry: slow growth, high fixed costs, perishable inventory, and transparent pricing. Rivalry management strategies include signaling intentions (avoiding misunderstanding that triggers retaliation), pursuing blue ocean strategies (creating uncontested market space), or consolidating through mergers to reduce competitor count.

6. Complementors (Sixth Force Extension)

Some strategists add complementors as a sixth force (Brandenburger & Nalebuff’s Co-opetition framework). Complementors are firms whose products increase demand for an industry’s products. Software developers complement hardware manufacturers (better software increases hardware demand); app stores complement smartphone makers; navigation apps complement automobile sales. Unlike substitutes (which reduce demand), complementors enhance industry profit potential. Industry attractiveness depends partly on complementor availability and quality. Strategies include: attracting complementors (open APIs, developer support programs), subsidizing complementors (below-cost pricing to build ecosystem), or integrating complementary products internally. Ignoring complementors leads to missed opportunities; treating complementors as rivals destroys ecosystem value. The smartphone industry’s success stems from robust complementor ecosystems (app developers, accessory makers, carriers) no single firm could have created all value alone.

7. Industry Structure as Determinant

Porter’s model emphasizes that industry structure—not just firm capabilities—systematically determines profitability. Structure refers to stable, enduring characteristics of an industry that shape competitive behavior: concentration (number and size distribution of firms), product differentiation (homogeneous vs. heterogeneous), entry/exit barriers, and vertical integration patterns. Structural analysis explains why average profitability differs systematically across industries (pharmaceuticals high, airlines low) regardless which firms compete. Managers often overattribute performance differences to firm strategy while underestimating structural effects. The strategic implication: choose industries with favorable structure (high barriers, low supplier/buyer power, few substitutes, moderate rivalry) rather than competing brilliantly in structurally unattractive industries. However, organizations can also influence structure through strategic actions—building entry barriers, reducing buyer power through differentiation, or consolidating to reduce rivalry.

8. Dynamic Competition and Force Interactions

The five forces are not independent; they interact dynamically. A technological change reducing entry barriers (new force) simultaneously intensifies rivalry (existing force). A merger increasing concentration (reducing rivalry) may also increase supplier power (combined firm has fewer supplier options). Regulatory change reducing buyer switching costs increases both buyer power and substitute threat. Strategic moves affect multiple forces simultaneously: product differentiation reduces buyer power and substitute threat but may increase rivalry (differentiated products compete on features, not price). Backward integration reduces supplier power but creates new entry barriers (capital requirements for integration deter entrants). Managers must analyze interactions, not treat forces in isolation. Static analysis (today’s forces) is insufficient; dynamic analysis examining how forces will evolve—and how strategic actions will change multiple forces simultaneously—distinguishes sophisticated from superficial industry analysis.