by

by Demand theory is a key principle in microeconomics that examines how consumers make decisions about purchasing goods and services based on price and other influencing factors. It explores the relationship between the price of a product and the quantity demanded by consumers over a specific period. The fundamental assumption is that, all other factors being equal, as the price of a product falls, demand increases, and as the price rises, demand decreases. This inverse relationship is represented by the demand curve, which typically slopes downward from left to right.

The core of demand theory lies in the concept of utility, or the satisfaction a consumer gains from consuming a product. Consumers allocate their limited income to maximize utility, and their willingness to purchase depends on how valuable they perceive the good to be in satisfying their needs. Thus, demand is influenced not only by price but also by income levels, tastes, preferences, and expectations.

Demand theory helps explain consumer behavior and the functioning of markets. It also distinguishes between a change in quantity demanded (movement along the curve due to price change) and a change in demand (shift of the curve due to non-price factors).

In practical terms, demand theory provides businesses and policymakers with tools to understand pricing, forecast demand, and make informed economic decisions. It plays a crucial role in achieving market equilibrium, where the quantity demanded equals the quantity supplied at a specific price.

The demand for a good or service depends on two factors:

- Its utility to satisfy a want or need.

- The consumer’s ability to pay for the good or service. In effect, real demand is when the readiness to satisfy a want is backed up by the individual’s ability and willingness to pay.

Built into demand are factors such as consumer preferences, tastes, choices, etc. Evaluating demand in an economy is, therefore, one of the most important decision-making variables that a business must analyze if it is to survive and grow in a competitive market. The market system is governed by the laws of supply and demand, which determine the prices of goods and services. When supply equals demand, prices are said to be in a state of equilibrium. When demand is higher than supply, prices increase to reflect scarcity. Conversely, when demand is lower than supply, prices fall due to the surplus.

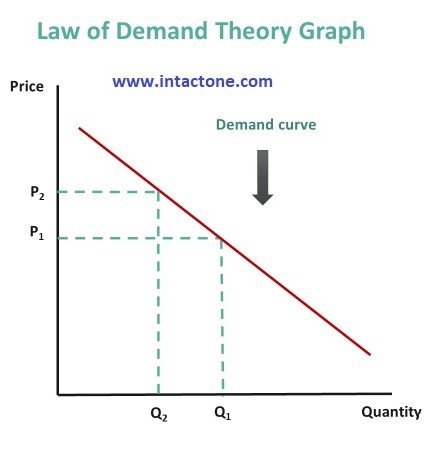

The law of demand introduces an inverse relationship between price and demand for a good or service. It simply states that as the price of a commodity increases, demand decreases, provided other factors remain constant. Also, as the price decreases, demand increases. This relationship can be illustrated graphically using a tool known as the demand curve.

The demand curve has a negative slope as it charts downward from left to right to reflect the inverse relationship between the price of an item and the quantity demanded over a period of time. An expansion or contraction of demand occurs as a result of the income effect or substitution effect. When the price of a commodity falls, an individual can get the same level of satisfaction for less expenditure, provided it’s a normal good. In this case, the consumer can purchase more of the goods on a given budget. This is the income effect. The substitution effect is observed when consumers switch from more costly goods to substitutes that have fallen in price. As more people buy the good with the lower price, demand increases.

Sometimes, consumers buy more or less of a good or service due to factors other than price. This is referred to as a change in demand. A change in demand refers to a shift in the demand curve to the right or left following a change in consumers’ preferences, taste, income, etc. For example, a consumer who receives an income raise at work will have more disposable income to spend on goods in the markets, regardless of whether prices fall, leading to a shift to the right of the demand curve.

Law of Demand:

Law of Demand is a fundamental principle in microeconomics that describes the inverse relationship between the price of a good or service and the quantity demanded by consumers, assuming all other factors remain constant (ceteris paribus). According to this law, when the price increases, the quantity demanded decreases, and when the price decreases, the quantity demanded increases.

This negative relationship occurs because of two key effects:

-

Income Effect – When prices fall, the consumer’s real income increases, enabling them to purchase more with the same budget.

-

Substitution Effect – A lower price makes a product more attractive compared to its substitutes, encouraging consumers to switch to the cheaper alternative.

The demand curve, which represents this law graphically, slopes downward from left to right, illustrating the declining demand as price rises.

The Law of Demand operates under certain assumptions:

-

Consumer income remains constant.

-

Tastes and preferences do not change.

-

Prices of related goods remain unchanged.

-

No expectations of future price changes exist.

While the law generally holds true, exceptions exist, such as:

-

Giffen goods – Inferior goods for which demand may rise as price rises.

-

Veblen goods – Luxury items whose higher prices may increase their desirability due to prestige.

In essence, the Law of Demand provides the basis for understanding consumer behavior and pricing mechanisms. It is crucial for business decisions, pricing strategies, and economic analysis, helping determine how changes in price can influence market demand.

Objectives of Demand theory:

- Understand Consumer Behavior

A primary objective of demand theory is to analyze consumer behavior in relation to changing prices and other factors. It helps economists and businesses understand why consumers buy more or less of a product. By studying this behavior, firms can adjust their offerings and marketing strategies to align with customer needs and preferences, ensuring better satisfaction and higher sales in competitive markets.

- Determine Demand Levels at Various Prices

Demand theory aims to estimate the quantity of goods or services consumers will purchase at different price points. This understanding helps businesses set optimal prices to maximize revenue. It also helps forecast how demand will change if prices are adjusted upward or downward, giving valuable input for inventory, production planning, and long-term business strategies in dynamic and price-sensitive markets.

- Formulate the Demand Curve

Another key objective is to develop a demand curve that illustrates the relationship between price and quantity demanded. The curve helps in visualizing and analyzing consumer responses to price changes. It also serves as a foundational tool in economic modeling, enabling businesses and policymakers to understand market mechanics and forecast trends based on price fluctuations or income variations.

- Identify Determinants of Demand

Demand theory seeks to identify and analyze the factors that influence demand, such as income, preferences, expectations, and prices of related goods. Understanding these determinants allows businesses and policymakers to anticipate changes in consumer behavior and respond accordingly. It ensures better planning, whether adjusting to market trends or implementing public policies that stimulate or control consumption.

- Facilitate Price Determination

Demand theory, along with supply theory, is instrumental in price determination under market conditions. By understanding the nature and magnitude of demand, economists can identify the equilibrium price—where supply equals demand. This helps maintain market balance and avoids issues like overproduction or shortages, enabling efficient resource allocation across industries and regions.

- Predict Market Changes

Demand theory helps in predicting how markets will react to changes in external factors such as price hikes, tax changes, or income fluctuations. With this predictive power, businesses and governments can prepare for demand shifts and make timely decisions. It also supports scenario planning, risk management, and the development of contingency strategies for unstable or changing economic environments.

- Guide Production and Inventory Decisions

One of the practical objectives is to guide production planning and inventory management. By understanding expected demand, firms can avoid overproduction or stockouts. This contributes to cost efficiency and customer satisfaction. Anticipating demand helps businesses adjust supply levels in line with consumer needs, reducing waste and optimizing operational flow.

- Aid in Policy and Economic Planning

Demand theory assists governments and institutions in framing economic and fiscal policies. By understanding public demand patterns, policymakers can implement programs like subsidies, taxation, or welfare measures more effectively. Demand analysis also helps in planning infrastructure, housing, transportation, and food security initiatives, ensuring that resources are distributed to match actual consumer needs.

Factors Affecting Demand:

- Price of the Good

The most direct factor influencing demand is the price of the good or service. According to the Law of Demand, when the price of a product increases, demand generally decreases, and vice versa. This inverse relationship occurs because higher prices reduce consumer purchasing power and make alternatives more attractive. However, exceptions like Giffen or Veblen goods may defy this trend due to unique consumer behavior or prestige value.

- Consumer Income

A rise in consumer income typically leads to an increase in demand for most goods, known as normal goods. Conversely, if income falls, demand for these goods declines. In contrast, inferior goods may see increased demand when income falls, as consumers substitute costlier items with cheaper alternatives. Thus, income changes directly affect purchasing power and shift the entire demand curve either to the right (increase) or left (decrease).

- Tastes and Preferences

Consumer tastes and preferences play a crucial role in shaping demand. Changes due to trends, advertising, health awareness, or cultural shifts can increase or decrease demand for specific products. For example, growing health consciousness may reduce demand for sugary beverages while increasing it for organic foods. These shifts are independent of price and can lead to a rightward or leftward shift in the demand curve based on changing consumer interests.

- Prices of Related Goods

The demand for a good is also influenced by the prices of related goods, such as substitutes and complements. If the price of a substitute rises (e.g., tea for coffee), demand for the original good increases. Conversely, if the price of a complement (e.g., printers and ink) rises, demand for the related good may fall. Thus, inter-product price relationships significantly affect consumer choices and overall market demand.

- Future Price Expectations

Consumer expectations of future prices influence current demand. If consumers expect prices to rise in the future, they may increase their current demand to avoid higher costs later. Conversely, if prices are expected to fall, current demand may decrease. This behavior is particularly evident in markets like real estate, fuel, or electronics, where future price movements are often anticipated based on trends or policy announcements.

- Number of Consumers

The size of the consumer base or market population also affects demand. An increase in the number of buyers—due to population growth, immigration, or market expansion—typically increases overall market demand. Conversely, a shrinking population or aging demographic may lead to lower demand for certain products. The larger the number of potential consumers, the higher the aggregate demand, assuming other factors remain constant.

- Government Policies and Taxation

Government actions, such as taxation, subsidies, or regulations, significantly influence demand. Higher taxes on goods (like tobacco or fuel) can reduce demand due to increased prices. Subsidies or tax rebates on essential or eco-friendly goods can encourage consumption. Regulatory decisions, such as bans or restrictions, may also directly affect demand levels in specific sectors by either discouraging or incentivizing purchases.

- Seasonal and Climatic Conditions

Demand is often affected by seasonal factors and climate conditions. Products like woolen clothes, air conditioners, umbrellas, or cold beverages experience fluctuating demand depending on weather or season. For instance, demand for winter wear spikes in cold months but drops in summer. Businesses must anticipate these cyclical changes to manage inventory and pricing effectively, as consumer preferences can be highly season-dependent.

Importance of Demand Analysis:

- Helps in Business Planning

Demand analysis is vital for effective business planning and decision-making. By understanding customer needs and expected sales volumes, firms can determine what to produce, in what quantity, and when. It minimizes guesswork and reduces the risk of overproduction or underproduction. With accurate demand insights, companies can align production schedules, manage resources efficiently, and make informed strategic decisions that contribute to profitability and long-term business sustainability.

- Assists in Pricing Strategy

One of the most important uses of demand analysis is in setting appropriate pricing strategies. It reveals how sensitive consumers are to price changes, known as price elasticity of demand. Understanding this sensitivity helps firms fix prices that maximize revenue without losing customers. Whether adopting premium pricing, discount pricing, or price skimming, demand analysis ensures that pricing aligns with consumer expectations and market conditions, improving competitiveness and profitability.

- Aids in Forecasting Future Demand

Demand analysis is essential for predicting future consumer behavior. By examining trends, past data, and current market conditions, businesses and policymakers can forecast how demand might change over time. Accurate demand forecasting supports inventory planning, resource allocation, and financial projections. It helps businesses respond proactively to market shifts, seasonal fluctuations, or changing economic conditions, ensuring readiness and continuity in uncertain or dynamic environments.

- Facilitates Inventory Management

Efficient inventory control depends on accurate demand analysis. By understanding which products are likely to be in demand, firms can stock appropriate quantities, reducing the risk of overstocking or stockouts. This prevents capital from being tied up in unsold goods and minimizes storage costs. Proper demand planning improves supply chain efficiency, supports timely order fulfillment, and enhances customer satisfaction by ensuring product availability when needed.

- Improves Marketing Effectiveness

Demand analysis provides insights into consumer preferences, behavior, and buying patterns, which are critical for designing targeted marketing campaigns. By understanding what consumers want and when, marketers can tailor promotional messages, select appropriate media, and time their campaigns for maximum impact. Demand insights also help identify market segments, guide product positioning, and evaluate the success of advertising efforts, ensuring a better return on marketing investments.

- Supports Resource Allocation

By identifying which products or services are in high demand, firms can allocate resources like labor, capital, and raw materials more effectively. Demand analysis ensures that businesses invest in the right areas and avoid wastage on low-performing segments. This leads to optimal utilization of financial and operational resources, improving productivity and cost-efficiency across the organization, especially in multi-product or seasonal businesses.

- Guides New Product Development

Demand analysis plays a crucial role in identifying unmet needs and evaluating the potential success of new products. It helps businesses innovate based on what consumers actually want. By assessing gaps in the market or tracking evolving preferences, firms can launch products that are more likely to succeed, reducing the risk of failure and enhancing customer satisfaction through relevant offerings.

- Informs Government Policy and Planning

Governments use demand analysis to design effective public policies and economic programs. Understanding public demand for goods, services, and infrastructure helps in budgeting, welfare planning, taxation, and subsidy allocation. It also aids in controlling inflation, ensuring food security, and managing public utilities. Demand data enables targeted interventions that improve social welfare and promote balanced economic growth.

2 thoughts on “Law of Demand”